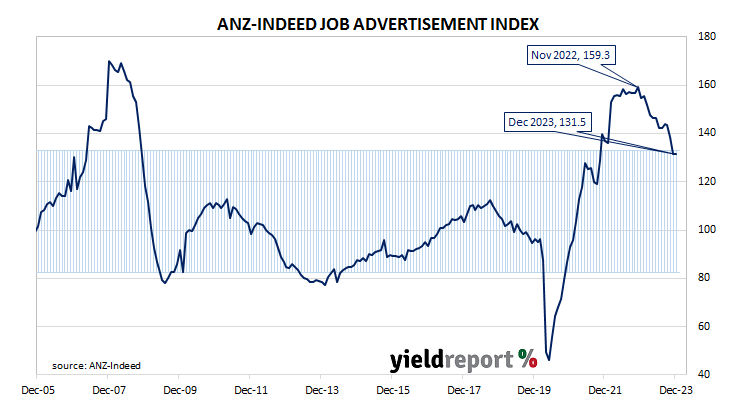

Summary: Job ads up 0.1% in December; 14.9% lower than December 2022; ANZ: 10.0% month-on-month fall in unadjusted terms; short-term ACGB yields fall, longer-terms steady/up modestly; rate-cut expectations soften slightly; ANZ: no signs of sharp deterioration approaching; ad index-to-workforce ratio steady.

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising and this trend continued into the first quarter of 2020. Advertising then plunged in April and May of 2020 as pandemic restrictions took effect but recovered quite quickly, reaching historically-high levels in 2022.

According to the latest ANZ-Indeed figures, total advertisements rose by 0.1% in December on a seasonally adjusted basis. The result followed losses of 5.1% in November and 3.4% in October. On a 12-month basis, total job advertisements were 14.9% lower than in December 2022, up from November’s revised figure of -17.5%.

“In original terms, there was a 10.0% month-on-month fall, reflecting the seasonal drop off in recruiting going into the holiday break,” said ANZ senior economist Catherine Birch.

Short-term Commonwealth Government bond yields fell on the day while long-term yields were either steady or modestly higher, somewhat similar to movements of US Treasury yields on Friday night. By the close of business, the 3-year ACGB yields had lost 2bps to 3.63%, the 10-year yield had returned to its starting point at 4.09% while the 20-year yield finished 3bps higher at 4.43%.

In the cash futures market, expectations regarding rate cuts later this year softened slightly. At the end of the day, contracts implied the cash rate would remain close to the current rate of 4.32% and average 4.32% through February, 4.31% in March and 4.295% in April. August contracts implied a 4.07% average cash rate while November contracts implied 3.88%, 44bps less than the current rate.

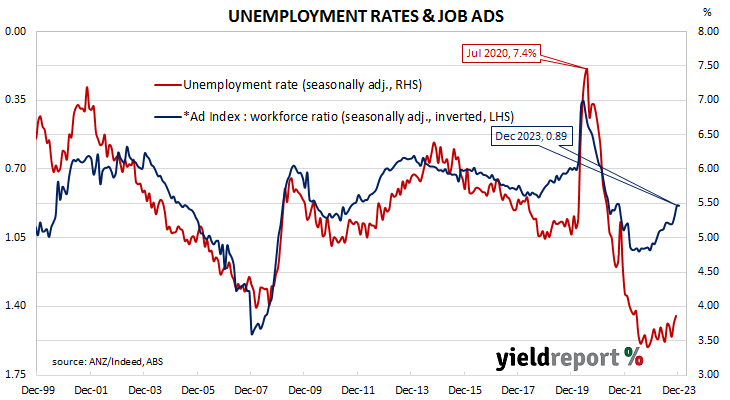

“ABS job vacancies only declined 0.7% quarter-on-quarter in November, adding to the evidence that while the labour market is easing, there are no signs of a sharp deterioration approaching,” Birch added. “Vacancies per unemployed person declined to 0.68, a two-year low, but this is still double the pre-COVID level.”

The inverse relationship between job advertisements and the unemployment rate has been quite strong (see below chart), although ANZ themselves called the relationship between the two series into question in early 2019. A higher job advertisement index as a proportion of the labour force is suggestive of lower unemployment rates in the near future while a lower ratio suggests higher unemployment rates will follow. December’s ad index-to-workforce ratio remained steady at 0.89 after revisions.

In 2008/2009, advertisements plummeted and Australia’s unemployment rate jumped from 4% to nearly 6% over a period of 15 months. When a more dramatic fall in advertisements took place in April 2020, the unemployment rate responded much more quickly.