13 July 2015

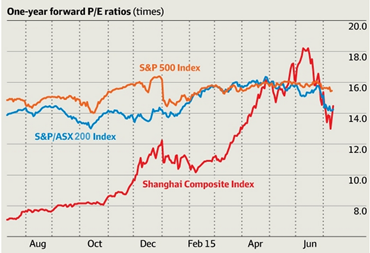

China’s stock markets suffered their biggest three week loss in twenty years after falling by nearly 10% on 2-3 July. In what has been interpreted as a ‘state’ intervention, the country’s 21 largest investment banks said they would spend about US$19.3 billion to try to stabilize the market and buy stocks themselves. They are being helped by the state-backed margin finance company, China Securities Finance Corp, which in turn would be aided by the PBOC. In addition, on Sunday, China state-owned investment company Central Huijin said it had recently been buying exchange-traded funds and would continue to do so.

In response, global debt markets moved considerably on Monday. Australian 3y and 10y bond rates dropped 11bps and 14bps respectively while US and German bond rates also fell considerably in what could be described as a flight to safety out of relatively more risky equity markets.

WBC’s senior international economist, Huw McKay, said it’s not “a threat to the Chinese financial system…the core of the banking system is relatively untouched” as it was securities firms who provided the margin lending. Chinese banks, in theory, are not allowed to lend for stockmarket activities but as the Economist noted recently “many will have, whether knowingly or not, and so will have a new category of bad debts to worry about.”

By the end of last week, yields had returned to where they started the week, although they were still down on the week.

13 July 2015

The IMF released its country report on the US last week and it projects GDP growth to be 2.5% for 2015, rising to 3.0% in 2016. The report also explained US first quarter weakness in terms of bad weather, a drop in oil sector investment and the West coast port strike. It then reiterated Christine Lagarde’s recent statements in advising the Federal Reserve to delay raising rates until there are further signs of wage or price inflation.

13 July 2015

The chair of Eurozone finance ministers, Jeroen Dijsselbloem, confirmed the receipt of Greece’s counteroffer of Greek economic reforms needed to qualify for further EU economic assistance. The reforms have not been made public and would be need to be approved by Greek parliamentarians before implementation should EU approval be given. It is thought a three year loan is involved but the Dutch minister would not comment until officials from the EU, ECB and IMF had made an assessment. It is thought more parties are coming around to the idea of some sort of “haircut” needs to be taken. The German finance minister said, “Debt sustainability is not feasible without a haircut and I think the IMF is correct in saying that.”

13 July 2015

The Greek government owes the European Stability Facility €40bn and €150bn to the ECB and various European central banks. All these institutions are funded or guaranteed by European countries’ governments. If there were a 100% write off of Greek government debts, these institutions would need recapitalising. Various European member states would then probably have to issue bonds. One country’s debts would simply become other countries’ debts.

13 July 2015

In 2009 the fear inspired by Greek budget problems was European private sector banks holding that country’s bonds would become insolvent as losses on the bonds mounted. This year the concern is not as great as the exposure in the private sector was much smaller. AMP’s chief economist Shane Oliver wrote recently “Greece is such as small part of the global economy, private sector exposure to Greece is small and neighbouring countries such as Spain, Italy and Portugal are in better shape than they were when doubts about Greece’s ability to pay the IMF started.”

13 July 2015

ANZ released its job ads figures last week. Job ads were up 1.3% compared to the previous month and 10.8% up from June, 2014. It is the latest in long string of positive figures. However the latest increase is lower than previous increases and an ANZ economist, Justin Fabo said the reduction in growth rates would be reflected in lower levels of job creation. ANZ’s Warren Hogan said he expected the first signs of weaker employment growth later in the week when the ABS Labour Force are released.

13 July 2015

In a report addressing potential financial benchmark rigging in Australia, ASIC provided what is called an “overview of the importance of financial benchmarks and the need for financial benchmarks to be robust and reliable” as well as some as the investigations ASIC is undertaking.

Benchmark interest rates are set by groups of banks, both domestic and foreign, through various mechanisms. These rates are then used as the starting point for pricing many financial instruments in the stock and bond markets and are often determinants of commercial lending rates and mortgage rates.

As the benchmarks are part of so many transactions, any manipulation of them has far-reaching effects throughout the Australian economy and financial markets. ASIC said several banks had given enforceable undertakings with regards to BBSW submissions after it was found some banks had engaged in practices which may have benefited “house” trading and derivatives positions.

13 July 2015

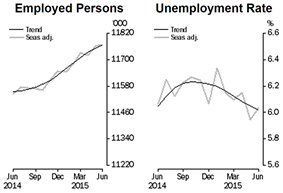

The ABS released the June Labour Force figures and, as with the May numbers, they were better than expected. The unemployment number came in at 6.0% as compared to the consensus expectation of 6.1% and May’s number has been revised down to 5.9% from the original 6.0% released a month ago. On top of these figures, the participation rate increased to 64.8% (seasonally adjusted) so the drop in unemployment does not appear to be a result of people giving up the search for work.

NSW and WA had the lowest rates of unemployment at 5.8% but WA’s rate deteriorated significantly from the 5.1% recorded in May. At the other end is SA and it suffered a further deterioration to 8.2% from the 7.6% recorded previously.

Commsec and ANZ said the latest ABS labour force figures were “better than expected”. CBA chief economist Michael Blythe said the figures indicated the economy was “in reasonable shape” while UBS believe the data will “give comfort to [the] RBA to hold rates”. However, UBS and others expressed some doubts over the statistical validity of the survey – doubts that have been dogging the ABS for nearly a year.

13 July 2015

Moody’s has assigned a first-time rating to Credit Union Australia (CUA) of A3. CUA already has a BBB+ rating with a stable outlook stable from S & P which it received in 2012. The investment grade rating was granted on the basis of CUA’s mutual ownership structure, strong asset quality and its common equity tier 1 ratio of 14.4%.

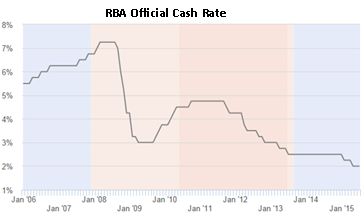

13 July 2015

The RBA held its regular first Tuesday of the month meeting and, as expected, kept the official cash rate steady. The AMP’s chief economist, Shane Oliver said afterwards he still thought there was “a 50/50 chance of another rate cut” while Westpac’s Bill Evans said, “Westpac’s current view is that rates will remain on hold through both 2015 and 2016.” CBA’s view is it expects the official rate to remain at “2.00% over the forecast horizon.”

One notable statement to come from the RBA release was the observation by the RBA governor, Glenn Stephens, “Despite… China and Greece, long-term borrowing rates for most sovereigns and creditworthy private borrowers remain remarkably low.”