31 August 2023

Summary: Private sector credit up 0.3% in July, in line with expectations; annual growth rate slows to 5.3%; Westpac: average monthly pace at 0.4%, mirrors housing market developments; UBS: slower trend since December 2022, will weaken further by end 2023; ACGB yields down moderately; rate-rise expectations soften; owner-occupier lending segment accounts for around 50% of net growth.

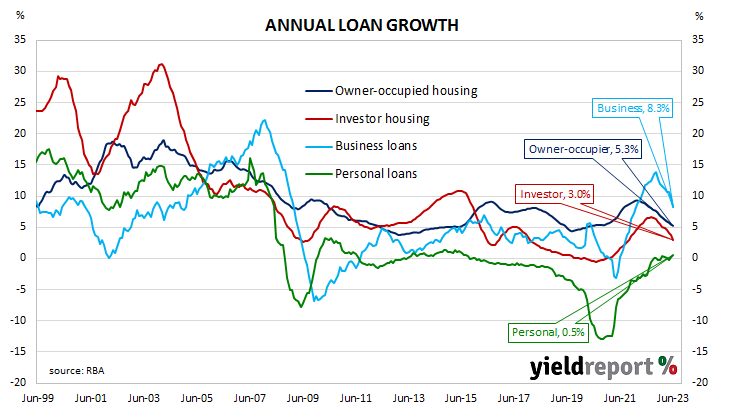

The pace of lending growth in the non-bank private sector by financial institutions in Australia followed a steady-but-gradual downtrend from late 2015 through to early 2020 before hitting what appears to be a nadir in March 2021. That downtrend ended later in that same year and annual growth rates shot up through 2022, peaking in September/October before easing over the first half of 2023.

According to the latest RBA figures, private sector credit increased by 0.3% in July. The result was in line with expectations as well as June’s result after it was revised up from 0.2%. On an annual basis, the growth rate slowed from June’s revised figure of 5.6% to 5.3%.

“In the 2023 year to date, the average monthly pace has held at 0.4%, albeit with some volatility month to month,” said Westpac senior economist Andrew Hanlan. “That stabilisation in the monthly pace mirrors developments in the housing market.”

The figures came out on the same day as June quarter capex figures and Commonwealth Government bond yields fell moderately across the curve. By the close of business, 3-year, 10-year and 20-year ACGB yield had all lost 5bps to 3.73%, 4.02% and 4.37% respectively.

In the cash futures market, expectations regarding further rate rises softened. At the end of the day, contracts implied the cash rate would barely change from the current rate of 4.07% and average 4.07% in September and 4.095% in October. February 2024 contracts implied a 4.175% average cash rate, as did May 2024 contracts, 11bps more than the current rate.

“Overall, credit growth has been on a slower trend since December 2022,” said UBS economist George Tharenou. “This is consistent with our long-held view, that continues to forecast housing, and total, credit growth will weaken further towards around 4% by the end of 2023.”

Owner-occupier lending accounted for just over half of the net growth over the month, while lending in the business segment accounted for around 40%. Investor lending and personal lending both increased in net terms and accounted for the balance.

The traditional driver of overall loan growth, the owner-occupier segment, grew by 0.3% over the month, down from the 0.4% growth rates registered in the previous three months. The sector’s 12-month growth rate slowed again, this time from 5.3% to 5.1%.

Total lending in the non-financial business sector increased by 0.3%, up from 0.2% in the previous month after revisions. Growth on an annual basis slowed from 8.3% to 7.6%.

Monthly growth in the investor-lending segment slowed to a near-halt in early 2018 and essentially stayed that way until mid-2021. In July, net lending rose by 0.2%, the same rate as in the previous three months, taking the 12-month growth rate from 3.4% after revisions to 3.2%.

Total personal loans rose by 0.5%, up from 0.1% in June, taking the annual growth rate from 0.5% to 0.9%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.