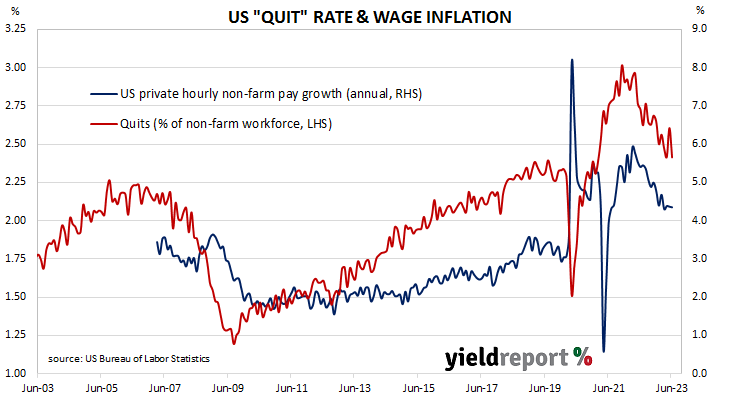

Summary: US quit rate falls to 2.4% in June; NAB: supports thesis wage disinflation achievable without outright job losses; US Treasury yields rise noticeably; expectations of Fed rate cuts in 2024 soften slightly; quits, separations, openings all down.

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in March 2019 and then tracked sideways until virus containment measures were introduced in March 2020. The quit rate then plummeted as alternative employment opportunities rapidly dried up. Following the easing of US pandemic restrictions, it proceeded to recover back to its pre-pandemic rate in the third quarter of 2020 and trended higher through 2021 before easing through 2022 and early 2023.

Figures released as part of the latest Job Openings and Labor Turnover Survey (JOLTS) report show the quit rate fell in June, maintaining its recent downtrend. 2.4% of the non-farm workforce left their jobs voluntarily, down from 2.6% in May. Quits in the month fell by 295,000 while an additional 209,000 people were employed in non-farm sectors.

“The JOLTS data supports Fed Governor Christopher Waller’s thesis that wage disinflation can be achieved without outright job losses,” said NAB senior FX strategist Rodrigo Catril.

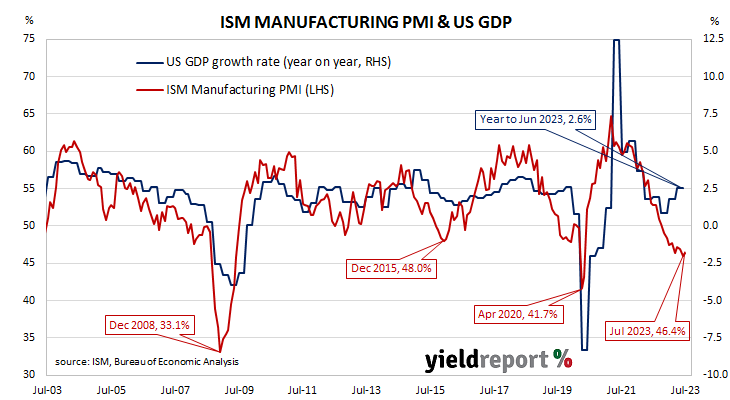

The figures were released on the same day as the latest ISM PMI report and US Treasury yields finished the day noticeably higher. By the close of business, the 2-year Treasury bond yields had added 6bps to 4.91%, the 10-year yield had gained 7bps to 4.03% while the 30-year yield finished 8bps higher at 4.09%.

In terms of US Fed policy, expectations of a lower federal funds rate in the first half of 2024 softened a touch. At the close of business, contracts implied the effective federal funds rate would average 5.33% in August, in line with the current spot rate, and then increase to an average of 5.345% in September. December futures contracts implied a 5.40% average effective federal funds rate while July 2024 contracts implied 4.905%, 42bps less than the current rate.

The fall in total quits was led by 95,000 fewer resignations in the “Retail trade” sector while the “Arts, entertainment, and recreation” sector experienced the largest gain, increasing by 20,000. Overall, the total number of quits for the month fell from May’s revised figure of 4.067 million to 3.772 million.

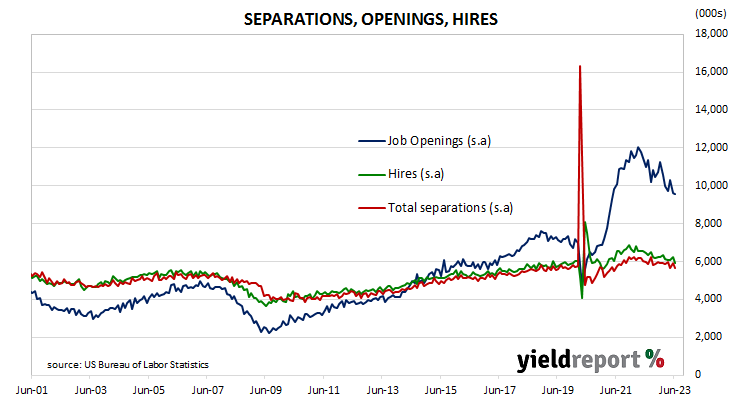

Total vacancies at the end of June declined by 34,000, or 0.4%, from May’s revised figure of 9.616 million to 9.582 million. The fall was driven by a 98,000 loss in the “Accommodation and food services” sector while the “Health care and social assistance” sector experienced the single largest increase, rising by 136,000. Overall, 11 out of 18 sectors experienced fewer job openings than in the previous month.

Total separations decreased by 288,000, or 4.9%, from May’s revised figure of 5.925 million to 5.637 million. The fall was led by the “Retail trade” sector where there were 134,000 fewer separations than in May. Separations increased in 13 of the 18 sectors.

The “quit” rate time series produced by the JOLTS report is a leading indicator of US hourly pay. As wages account for around 55% of a product’s or service’s price in the US, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief and current Treasury Secretary Janet Yellen was known to pay close attention to it.