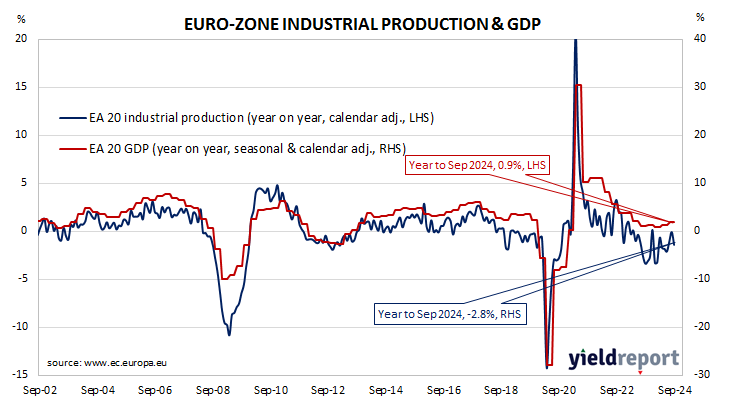

12 November 2024

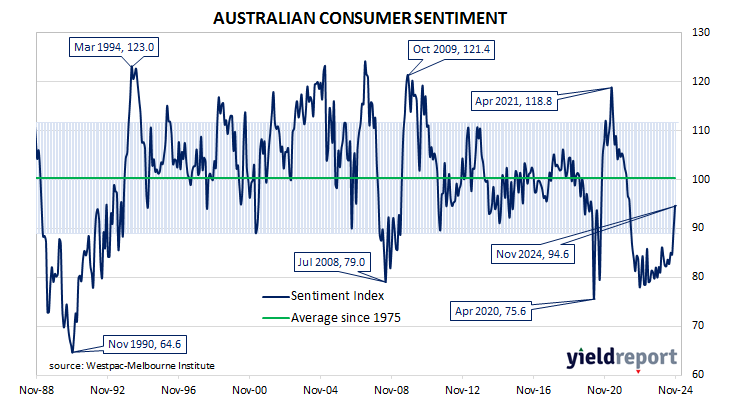

Summary: Westpac-Melbourne Institute consumer sentiment index rises in November; Westpac: consumers seeing some further easing in pressure on family finances, more confident about economic outlook; short-term ACGB yields increase, longer-term yields decline; rate-cut expectations soften; Westpac: sentiment posted sharp fall following US election, tentative recovery later in week; all five sub-indices rise; fewer respondents expecting higher jobless rate.

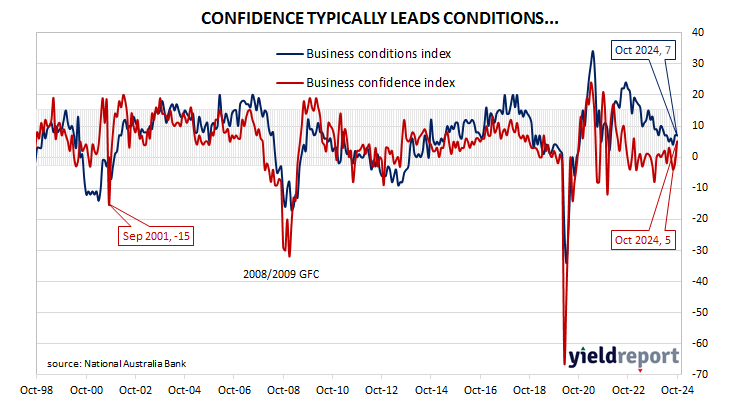

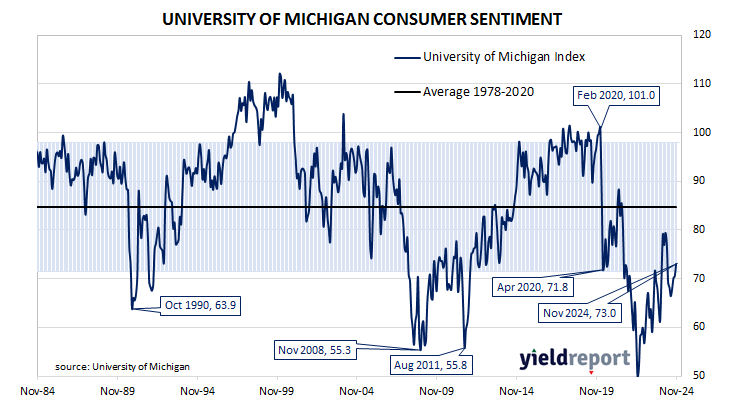

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment then weakened considerably and languished at pessimistic levels from mid-2022 while business sentiment generally remained at more robust levels.

According to the latest Westpac-Melbourne Institute survey conducted over the first week of November, household sentiment again improved markedly, albeit to a level which is still somewhat on the pessimistic side. Their Consumer Sentiment Index jumped from October’s reading of 89.8 to 94.6, a reading which is still lower than the long-term average reading of just over 101.

“Consumers are seeing some further easing in the pressure on family finances, are no longer concerned about the risk of further interest rate rises and are becoming more confident about the economic outlook,” said Westpac senior economist Matthew Hassan. “However, some big shifts over the course of the survey week suggest the lift in confidence is shakier than it looks.”

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

The figures came out on the same day as the latest NAB Business Survey and short-term Commonwealth Government bond yields increased modestly while longer-term declined a little. By the close of business, the 3-year ACGB yield had added 1bp to 4.11%, the 10-year yield had slipped 1bp to 4.58% while the 20-year yield finished 2bps higher at 4.88%.

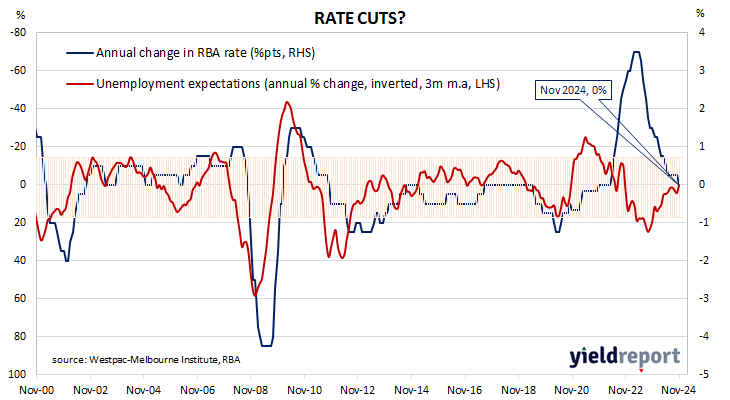

Expectations regarding rate cuts in the next twelve months softened, with a February cut now viewed as not especially likely. Cash futures contracts implied an average of 4.335% in November, 4.315% in December and 4.29% in February 2025. October 2025 contracts implied 3.96%, 38bps less than the current cash rate.

“Three things stand out,” Hassan added. “Firstly, consumer sentiment was markedly higher at the start of the week with an index read of 99.7 amongst those surveyed prior to the RBA announcement. Secondly, sentiment was unaffected by the RBA decision, with the index unchanged on November 5. Thirdly, sentiment posted a sharp fall following the US election result but with a tentative recovery forming towards the end of the week, with an average index read of 91.1 amongst responses gathered between November 6 and November 9.”

All five sub-indices registered higher readings, with the “Economic conditions – next 12 months” sub-index again posting the largest monthly percentage gain.

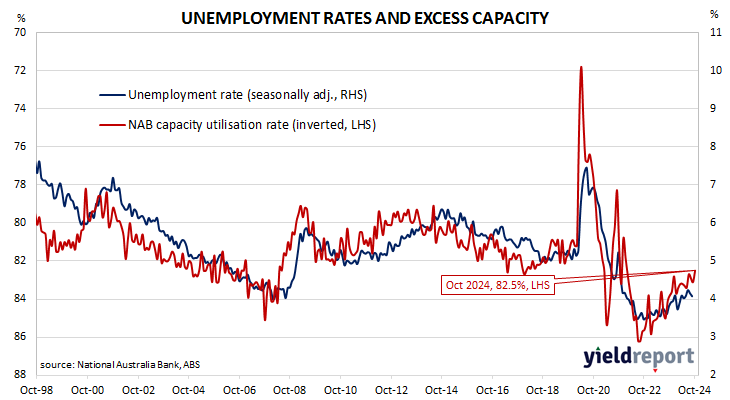

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, fell from 129.8 to 120.5, materially below the long-term average of 129.1. Lower readings result from fewer respondents expecting a higher unemployment rate in the year ahead.