03 May 2022

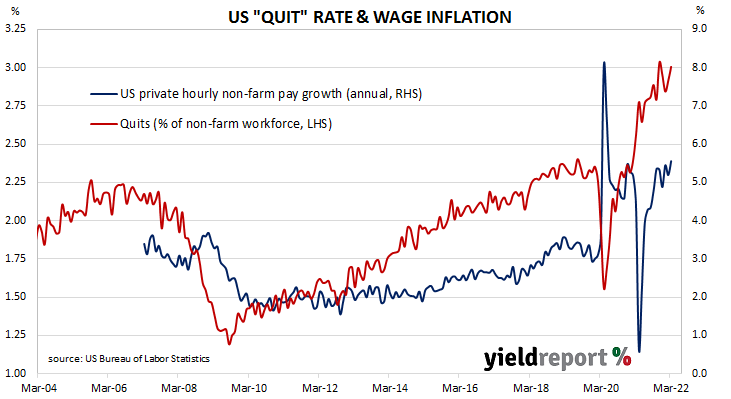

Summary: US quit rate up in March; labour market “extremely tight”; record high for quits series; quits, openings, separations all up.

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in March 2019 and then tracked sideways until virus containment measures were introduced in March 2020. The quit rate then plummeted as alternative employment opportunities rapidly dried up. Following the easing of US pandemic restrictions, it proceeded to recover back to its pre-pandemic rate in the third quarter of 2020 before trending higher through 2021.

Figures released as part of the most recent Job Openings and Labor Turnover Survey (JOLTS) report show the quit rate ticked up again in March. 3.0% of the non-farm workforce left their jobs voluntarily, up from February’s figure of 2.9%. There were 152,000 more quits during the month; this increase outweighed an additional 418,000 people employed in the non-farm sector in percentage terms.

“The [US] labour market is extremely tight and is a major focus for the Fed as it realigns supply and demand in order get inflation sustainably down to target,” said ANZ Head of Australian Economics David Plank. “The strength in demand for jobs was supplemented by a record high in the quits series, often interpreted as a barometer of workers’ willingness to quit and find better opportunities.”

Short-term US Treasury yields moved higher while longer-term yields fell. By the close of business, the 2-year Treasury bond yield had gained 4bps to 2.76%, the 10-year yield had slipped 1bp to 2.97% while the 30-year yield finished 2bps lower at 3.01%.

In terms of US Fed policy, expectations for a higher federal funds rate over the next 12 months firmed. At the close of business, May contracts implied an effective federal funds rate of 0.78%, 45bps higher than the current spot rate. July contracts implied 1.485% and March 2023 futures contracts implied an effective federal funds rate of 3.135%, 280bps above the spot rate.

The rise in total quits was led by 88,000 more resignations in the “Professional and business services” sector while the Construction sector was not far behind with 69,000 more quits. The “Health care and social assistance” sector experienced the single largest fall, declining by 19,000. Overall, the total number of quits for the month rose from February’s revised figure of 4.384 million to 4.536 million.

Total vacancies at the end of March increased by 205,000, or 1.8%, from February’s revised figure of 11.344 million to 11.549 million. The rise was driven by a 155,000 jump in the “Retail trade” sector and a 103,000 increase in the “Professional and business services” sector. The “Transportation, warehousing, and utilities” sector experienced the single largest decrease, falling by 69,000. Overall, 11 out of 18 sectors experienced more job openings than in the previous month.

Total separations increased by 239,000, or 3.9%, from February’s revised figure of 6.082 million to 6.321 million. The rise was led by the “Professional and business services” sector where there were 76,000 more separations than in February. Separations increased in 12 out of 18 sectors.

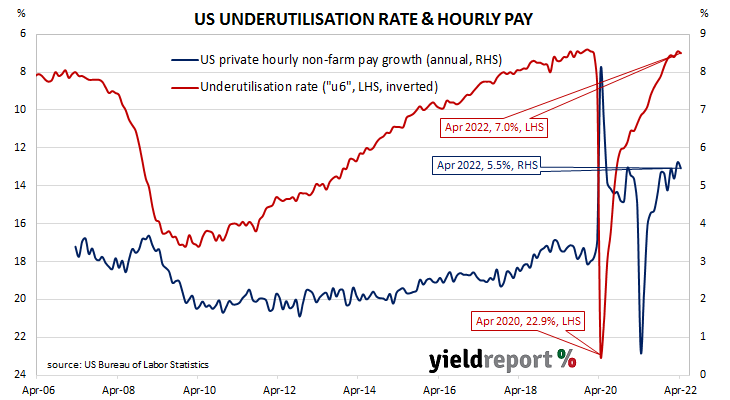

The “quit” rate time series produced by the JOLTS report is a leading indicator of US hourly pay. As wages account for around 55% of a product’s or service’s price in the US, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief and current Treasury Secretary Janet Yellen was known to pay close attention to it.