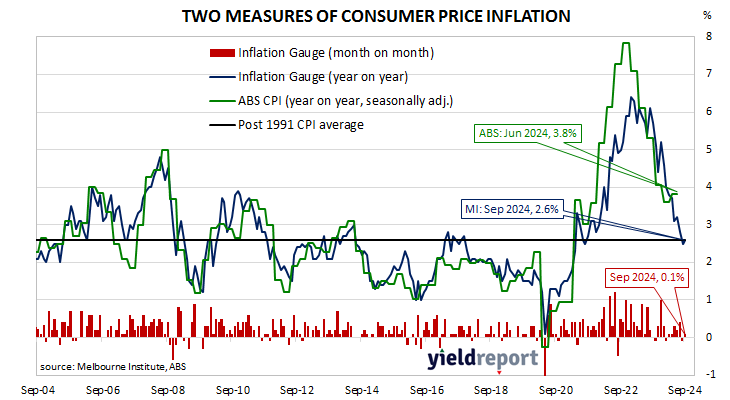

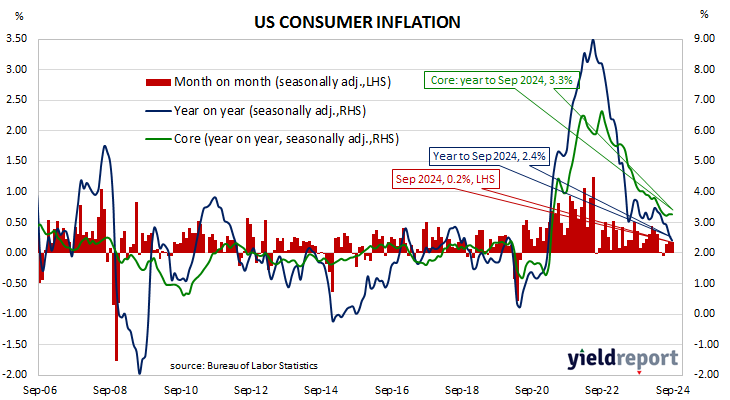

Summary: US CPI up 0.2% in September, in line with expectations; annual inflation rate slows from 2.6% to 2.4%; “core” rate up 0.3%, up 3.3% over year; Westpac: report a reminder inflation is down but not yet out; US Treasury yields generally fall; rate-cut expectations firm; non-energy services again main driver of overall result.

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. Substantially lower rates were reported from March 2020 to May 2020 and they remained below 2% until March 2021. They then rose significantly before declining from mid-2022.

The latest US CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by 0.2% on average in September. The rise was slightly above the 0.2% increase which had been generally expected but it was in line with increases in July and August. On a 12-month basis, the inflation rate slowed from 2.6% to 2.4%.

“Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. The core prices index, the index which excludes the more variable food and energy components, increased by 0.3% on a seasonally-adjusted basis over the month, above the 0.2% rise which had been generally expected but in line with August’s rise. The annual growth rate remained steady at 3.3%.

“A marginally hotter-than-expected US inflation report was a reminder that inflation is down but not yet out, supporting a more gradual pace of policy easing,” said Westpac economist Jameson Coombs.

US Treasury bond yields generally fell on the day, the exception being ultra-long yields which rose modestly. By the close of business, the 2-year Treasury yield had shed 6bps to 3.96%, the 10-year yield had slipped 1bp to 4.06% while the 30-year yield 2bps higher at 4.36%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months firmed, with at least another six 25bp cuts priced in. At the close of business, contracts implied the effective federal funds rate would average 4.665% in November, 17bps less the current rate, 4.515% in December and 4.175% in February. September 2025 contracts implied 3.50%, 133bps less than the current rate.

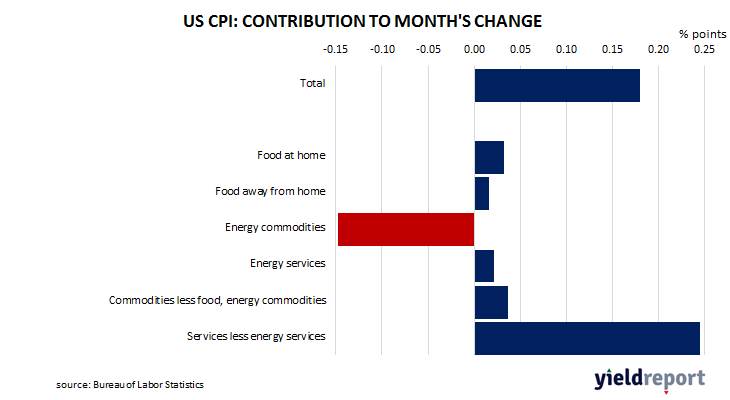

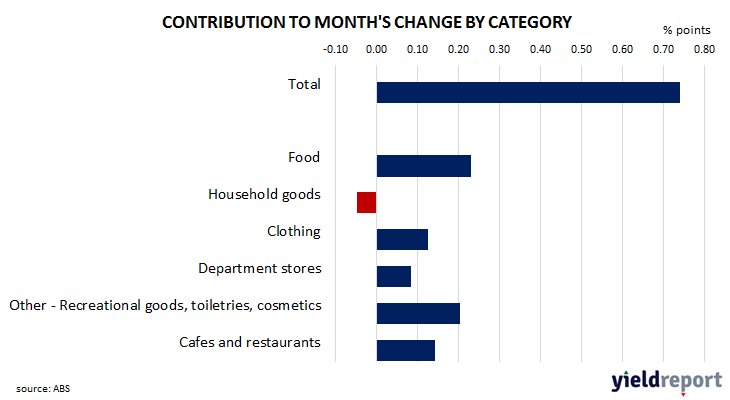

The largest influence on headline results is often the change in fuel prices. Prices of “Energy commodities”, the segment which contains vehicle fuels, decreased by 0.4% and contributed -0.15 percentage points to the total. However, prices of non-energy services, the segment which includes actual and implied rents, again had the largest single effect on the total as they contributed 0.25 percentage points following a 0.4% increase on average.