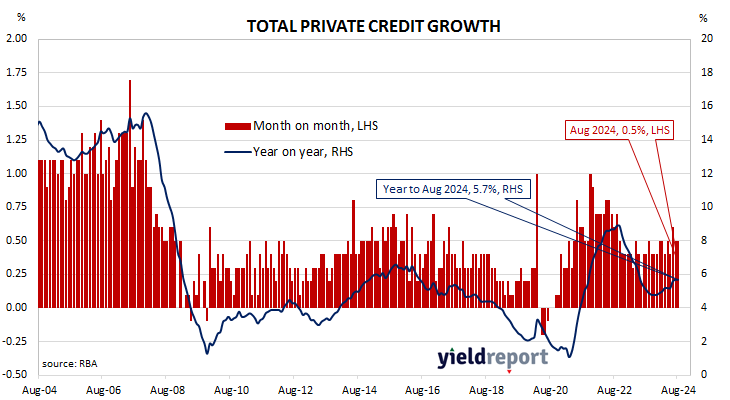

Summary: Private sector credit up 0.5% in August, in line with expectations; annual growth rate steady at 5.7%; Westpac: credit growth momentum firm and steady, above pre-pandemic levels; ACGB yields rise; rate-cut expectations soften, February cut still priced in; Westpac: still insufficient to generate a stronger GDP impulse; owner-occupier segment accounts for 50% of net growth.

The pace of lending growth in the non-bank private sector by financial institutions in Australia followed a steady-but-gradual downtrend from late 2015 through to early 2020 before hitting what appears to be a nadir in March 2021. That downtrend ended later in that same year and annual growth rates shot up through 2022, peaking in September/October before easing through 2023.

According to the latest RBA figures, private sector credit increased by 0.5% in August. The result was in line with expectations as well as July’s rise. On an annual basis, the growth rate remained unchanged at 5.7%.

“Stepping back, momentum in credit growth appears to be firm and stable,” said Westpac senior economist Mantas Vanagas. “It is comfortably above the pre-pandemic levels when interest rates were significantly lower.”

Commonwealth Government bond yields moved modestly higher across the curve. By the close of business, the 3-year ACGB yield had inched up 1bp to 3.46% while 10-year and 20-year yields both finished 2bps higher at 4.00% and 4.43% respectively.

Expectations regarding rate cuts in the next twelve months softened a little, albeit with a February 2025 rate cut still fully priced in. Cash futures contracts implied an average of 4.30% in November, 4.205% in December and 4.08% in February 2025. August 2025 contracts implied 3.395%, 94bps less than the current cash rate.

“However, against the backdrop of weak aggregate demand, it is still insufficient to generate a stronger GDP impulse,” Vanagas added. “And with household and business sentiment surveys remaining subdued, a similar dynamic is expected to persist in the near term.”

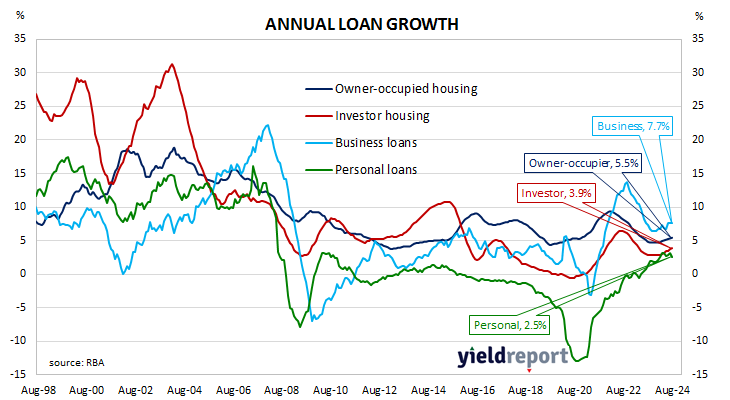

Owner-occupiers accounted for just over 50% of the net growth over the month while business lending accounted for slightly more than 35%. Investor lending accounted for almost all the balance.

The traditional driver of overall loan growth, the owner-occupier segment, grew by 0.4% over the month, slightly slower than July’s 0.5% rise. The sector’s 12-month growth rate ticked up from 5.4% to 5.5%.

Total lending in the non-financial business sector increased by 0.7%, up from July’s growth rate of 0.5%. Growth on an annual basis remained unchanged at 7.7%.

Monthly growth in the investor-lending segment slowed to a near-halt in early 2018 and essentially stayed that way until mid-2021. In August, net lending rose by 0.4%, as it had in each of the preceding four months. The 12-month growth rate increased from 3.7% to 3.9%.

Total personal loans increased by 0.1%, down from July’s 0.5% increase, while the annual growth rate slowed from 3.1% to 2.5%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.