Summary: Business conditions improve modestly in August; confidence also up slightly; confidence index reflects sharp deterioration in Victoria and degree of uncertainty in economy as lockdowns persist; tentative signs Delta outbreak and latest round of lockdowns having a less damaging economic impact than initial lockdown; capacity utilisation rate declines again; five of eight sectors of economy still at/above respective long-run averages.

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip, declining to below-average levels by the end of 2018. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and the index trended lower, hitting a nadir in April 2020 as pandemic restrictions were introduced. Conditions improved markedly over the next twelve months, only to fall markedly in June and July.

According to NAB’s latest monthly business survey of over 500 firms conducted over the last two weeks of August, business conditions improved modestly. NAB’s conditions index registered 14, up from July’s revised reading of 10.

Business confidence also improved slightly after three consecutive months of falls. NAB’s confidence index rose from July’s revised reading of -7 to -5, still well below the long-term average. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

NAB senior economist Gareth Spence said the confidence index’s negative reading reflects “a sharp deterioration in Victoria and more generally, the degree of uncertainty in the economy as lockdowns persist and the timing of a full re-opening remains unknown.”

Commonwealth Government bond yields fell noticeably on the day. By the end of it, the 3-year ACGB yield had lost 5bps to 0.22% while 10-year and 20-year yields each finished 7bps lower at 1.19% and 1.83% respectively.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, remained largely unchanged. At the end of the day, contract prices implied the cash rate would rise very gradually to around 0.21% by December 2022.

“There are tentative signs that the Delta outbreak and latest round of lockdowns…are having a less damaging economic impact than the initial lockdown in the first half of 2020,” said Westpac senior economist Andrew Hanlan. “On this occasion the lockdown is not nationwide, albeit it is the two largest states that are in lockdown. Leading into the latest lockdowns, the economy had considerable momentum, in contrast to the already sluggish conditions prior to the initial lockdown [of 2020].”

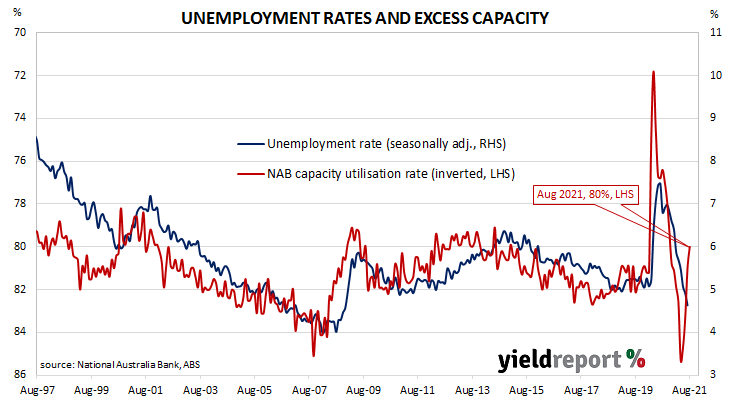

NAB’s measure of national capacity utilisation indicated it had declined again, falling from July’s revised figure of 81.0% to 80.0%. Even so, five of the eight sectors of the economy were reported to be still operating at or above their respective long-run averages, with the transport/utilities, retail and recreation/personal services sectors operating at below average levels.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.