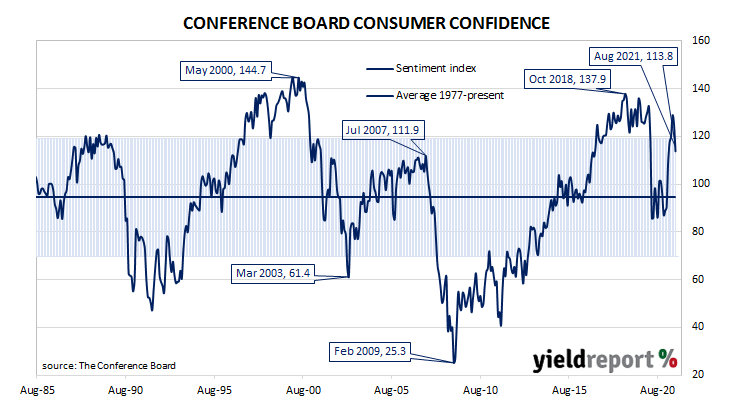

Summary: Noticeable fall in Conference Board Consumer Confidence Index in August; reading well below expected figure; views of present conditions, short-term outlook both less positive; Delta, rising gas and food prices results in less favourable views; US consumer “much less ebullient“ than earlier in year.

After the GFC in 2008/09, US consumer confidence clawed its way back to neutral over a number of years and then went from strength to strength until late 2018. Measures of consumer confidence then oscillated within a fairly narrow band at historically high levels until they plunged in early 2020. Subsequent readings then fluctuated around the long-term average until March this year when they reached elevated levels.

The latest Conference Board survey held during the first three weeks of August indicated US consumer confidence has noticeably deteriorated. August’s Consumer Confidence Index registered a preliminary reading of 113.8, well below the median consensus figure of 124.0 and July’s final figure of 125.1.

Consumers’ views of present conditions and their outlook for the near-future were both less positive. The Present Situation Index fell from 157.2 to 147.3 while the Expectations Index decreased from 103.8 to 91.4.

“Concerns about the Delta variant and, to a lesser degree, rising gas and food prices, resulted in a less favourable view of current economic conditions and short-term growth prospects,” said Lynn Franco, a senior director at The Conference Board. However, while US households had “cooled somewhat” some of their spending intentions, she also noted “the percentage of consumers intending to take a vacation in the next six months continued to climb.”

US Treasury bond yields increased on the day. By the close of business, the 2-year Treasury bond yield had inched up 1bp to 0.21% while 10-year and 30-years each gained 4bps to 1.31% and 1.93% respectively.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months remained low. Federal funds futures contracts for August 2022 implied an effective federal funds rate of 0.12%, about 6bps above the current spot rate.

“At 113.8, down from a downward-revised 125.1 in July, this was a lot weaker than expected and corroborates the message from the earlier University of Michigan readings that the US consumer is much less ebullient than earlier in the year,” said Ray Attrill, NAB’s Head of FX Strategy within its FICC division.

The Consumer Confidence Survey is one of two monthly US consumer sentiment surveys which result in the construction of an index. The Conference Board’s index is based on perceptions of current business and employment conditions, as well as respondents’ expectations of conditions six months in the future. The other survey, conducted by the University of Michigan, is similar and it is used to produce an Index of Consumer Sentiment. That survey differs in that it also includes some longer-term questions.