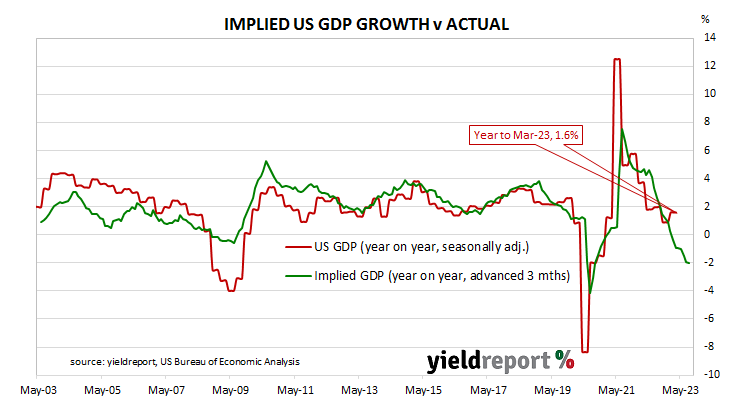

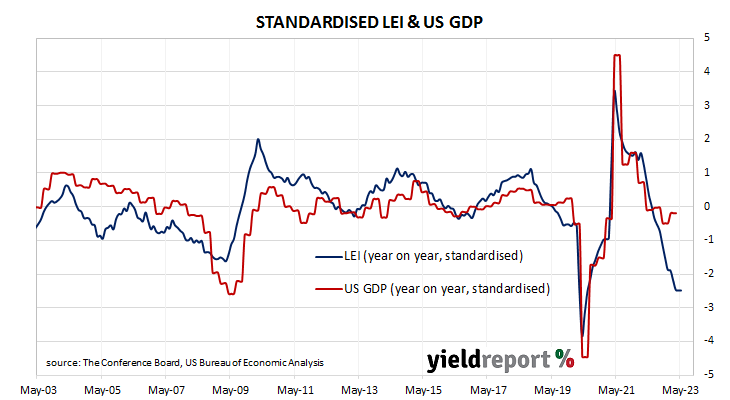

Summary: Conference Board leading index down 0.7% in May, fall slightly better than expected; index down for 14 consecutive months; regression analysis implies 2% contraction in year to August.

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April of 2020 signalled “a deep US recession” while subsequent readings indicated the US economy would recover rapidly. More recent readings have implied US GDP growth rates will turn negative sometime in 2023.

The latest reading of the LEI indicates it decreased by 0.7% in May. The result was slightly better than the expected -0.8% but it was also below April’s -0.6%.

“The US Leading Index has declined in each of the last fourteen months and continues to point to weaker economic activity ahead,” said Justyna Zabinska-La Monica of The Conference Board. “Rising interest rates paired with persistent inflation will continue to further dampen economic activity.”

US Treasury bond yields rose on the day, as Fed chief Jerome Powell continued his testimony to the US Congress. By the close of business, 2-year and 10-year Treasury yields had both gained 7bps to 4.79% and 3.80% respectively while the 30-year yield finished 6bps higher at 3.87%.

In terms of US Fed policy, expectations of a lower federal funds rate in 2024 softened noticeably. At the close of business, contracts implied the effective federal funds rate would average 5.11% in July, 3bps more than the current spot rate, and then increase to an average of 5.26% in August. December futures contracts implied a 5.31% average effective federal funds rate while June 2024 contracts implied 4.745%, 33bps less than the current rate.

“While we revised our Q2 GDP forecast from negative to slight growth, we project that the US economy will contract over the Q3 2023 to Q1 2024 period,” said Zabinska-La Monica. “The recession likely will be due to continued tightness in monetary policy and lower government spending.”

Regression analysis suggests the latest reading implies a -2.0% year-on-year growth rate in August, unchanged from July’s figure.