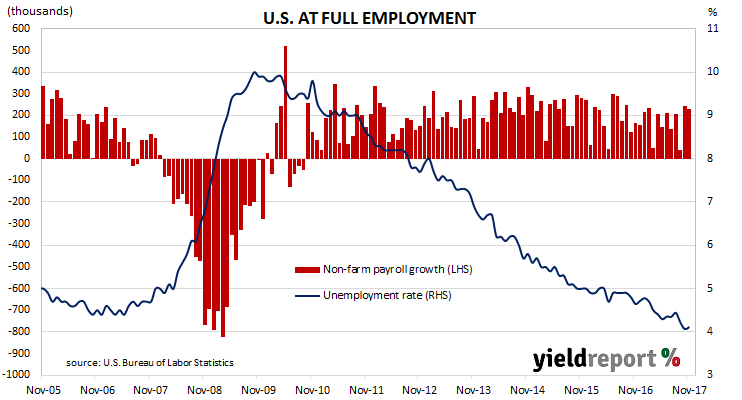

The U.S economy has managed to maintain a rate of unemployment which is the lowest for the period since February 2001. According to the U.S. Bureau of Labor Statistics, the U.S. economy gained 228,000 jobs in the non-farm sector in November while October’s figure was revised down from +261,000 to +244,000 but the September number was revised up from +18,000 to +38,000. The market’s median expectation for employment growth in November was +210,000.

After revisions to previous months’ figures, the unemployment rate remained unchanged at 4.1% as 90,000 either found work, retired or stopped looking for work. Average hourly pay rates reversed a dip in October and was 2.5% higher than in November 2016.

The total number of employed persons in the non-farm sector at the end of November was 147.2 million and 153.9 million overall. Over the past twelve months, 1.9 million jobs have been created in the U.S. with almost all of them in the non-farm sector. Another figure which is indicative of the state of the U.S. economy is the employment-to-population ratio. After a volatile few months, this ratio has settled down and came in at 60.1% for a second month in a row.

ANZ senior economist Felicity Emmett described the figures as “solid” but then she went on to focus on the wage inflation issue. “In a nutshell, economic and employment momentum remain very solid, but wage growth is subdued in the context of the broader environment….inflation expectations [are] well anchored, technological change, global integration of supply chains, increased labour mobility and low global inflation.”

Financial market reaction was unremarkable. The U.S. 2 year yield remained steady at 1.79% while the 10 year yield gained 1bp to 2.37%. The U.S currency was slightly stronger against the yen but steady against the euro. According to cash futures prices, the implied probability of a rate rise by the U.S. FOMC at its upcoming December meeting was unchanged at 100%.