The NSW government budget was delivered last week and it announced a headline surplus of $2.1bn (vs $0.3bn previously). The 2015/16 borrowing requirement would be $7.3bn and this compares to the $4.3bn NSWTC requirement in 2014/15.

NSW is rated AAA/Aaa by S&P and Moody’s and after the budget was tabled, both Moody’s and S&P immediately stated NSW’s rating would not be affected.

The budget showed surging revenues from property stamp duties with nearly $2.0bn more than previously forecast and reinforcing the market’s view of NSW’s and Victoria’s superior fiscal positions to other states.

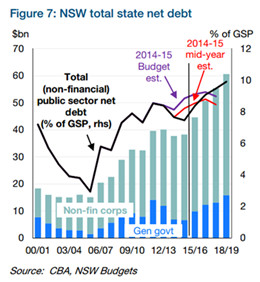

NSW faces an ongoing large capital spending outlook, which is a key source of fiscal risk for the state. Net debt is forecast to grow from $9.9b in 2015/2016 to $15.8b in 2018/2019 but essentially the NSW government has an operating surplus. The government is undertaking a 99y lease of 49% of its electricity transmission and distribution business although the proceeds are not included in the Budget until realised. The budget forecasts $30b in sales proceeds but $20b is earmarked for the “Rebuilding NSW” program leaving a forecast net $10bn for debt reduction.