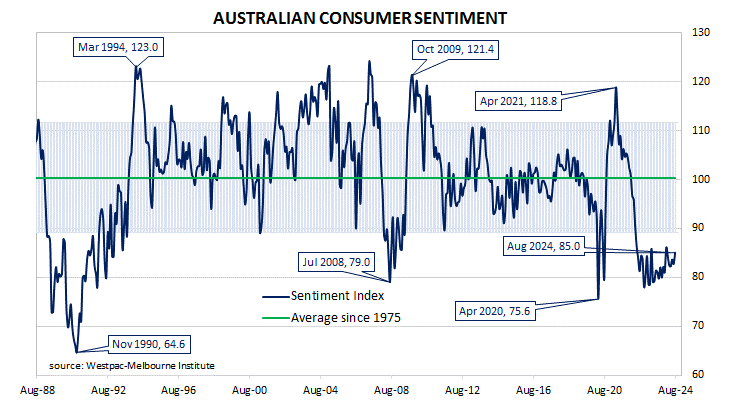

Summary: Westpac-Melbourne Institute consumer sentiment index rises in August; Westpac: consumers relieved as RBA leaves interest rates unchanged, support from tax cuts, other fiscal measures becomes apparent; ACGB yields fall moderately; rate-cut expectations firm; Westpac: rate rise fears subsided noticeably in month; four of five sub-indices rise; more respondents expecting higher jobless rate.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment then weakened considerably and has languished at pessimistic levels since mid-2022 while business sentiment has been more robust.

According to the latest Westpac-Melbourne Institute survey conducted over the first full week of August, household sentiment has improved, albeit to a level which is still quite pessimistic. Their Consumer Sentiment Index increased from July’s reading of 82.7 to 85.0, a reading which is significantly lower than the long-term average reading of just over 101 and well below the “normal” range.

“Consumers breathed a small sigh of relief in August as the RBA Board left interest rates unchanged and the support coming from tax cuts and other fiscal measures became more apparent,” said Westpac senior economist Matthew Hassan.

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

Domestic Treasury bond yields fell moderately across the curve on the day, largely in line with movements of US Treasury yields on Monday night. By the close of business, the 3-year ACGB yield had lost 4bps to 3.60%, the 10-year yield had shed 5bps to 4.01% while the 20-year yield finished 3bps lower at 4.40%.

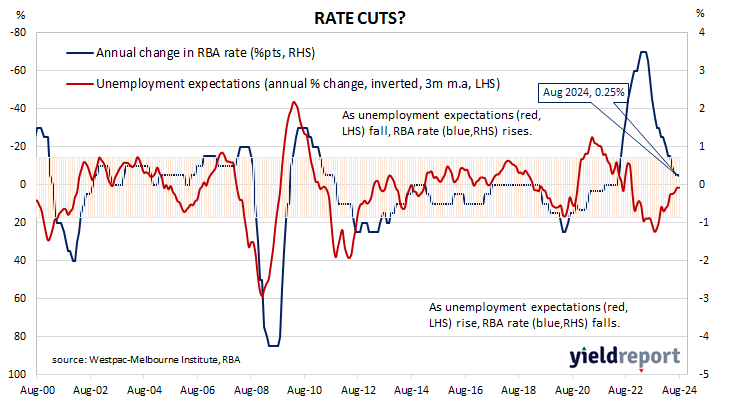

Expectations regarding rate cuts in the next twelve months firmed, with a February 2025 rate cut fully priced in. Cash futures contracts implied an average of 4.32% in September, 4.285% in October and 4.20% in November. February 2025 contracts implied 4.03% while July 2025 contracts implied 3.63%, 71bps less than the current cash rate.

“Rate rise fears subsided noticeably in the month,” added Hassan, “Notably, about 10% of that move came before the RBA announced its decision to leave interest rates on hold in August, suggesting rate rise fears had already eased significantly following the June quarter inflation update, and perhaps in response to a clearer signs of a monetary-easing cycle emerging abroad.”

Four of the five sub-indices registered higher readings, with the “Family finances versus a year ago” sub-index posting the largest monthly percentage gain.

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 128.6 to 133.5, slightly above the long-term average. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.