Summary: Household sentiment improves significantly for second consecutive month; confidence index back to above long-term average; “an extraordinary result”; at level last seen in late 2018; index higher in all states, all components higher; “stunning lift” in job security confidence.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April but, after a few months of to-ing and fro-ing, then staged a considerable recovery.

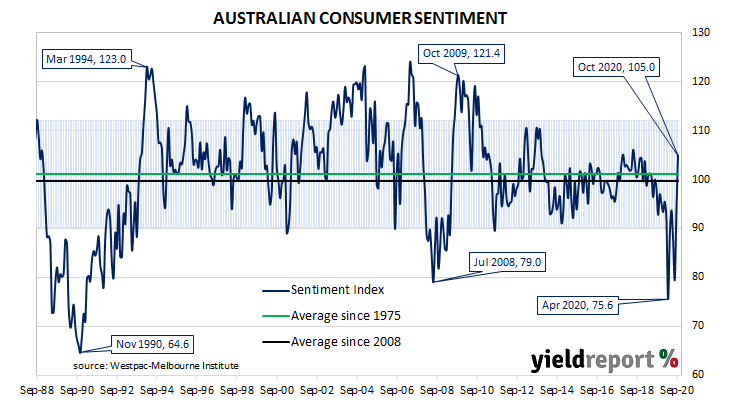

According to the latest Westpac-Melbourne Institute survey conducted in early October, household sentiment has increased markedly. The Consumer Sentiment Index jumped for a second consecutive month, this time from September’s 93.8 to 105.0, taking it back to above-average levels.

“This is an extraordinary result,” said Westpac chief economist Bill Evans.

Local Treasury bond yields rose a touch at the short end but declined a little elsewhere. By the end of the day, the 3-year ACGB yield had crept up 1bps to 0.19% while 10-year and 20-year yields both finished 1bp lower at 0.84% and 1.43% respectively.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to favour a slight easing. At the end of the day, contract prices implied the cash rate would trade in a range between 0.06% and 0.08% through to the end of 2021.

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure has moved back to levels last seen in late 2018, above the long-term average reading of just over 101.

Evans noted confidence had increased in all states and all components of the index were higher. He also noted “a stunning lift in confidence around job security.”