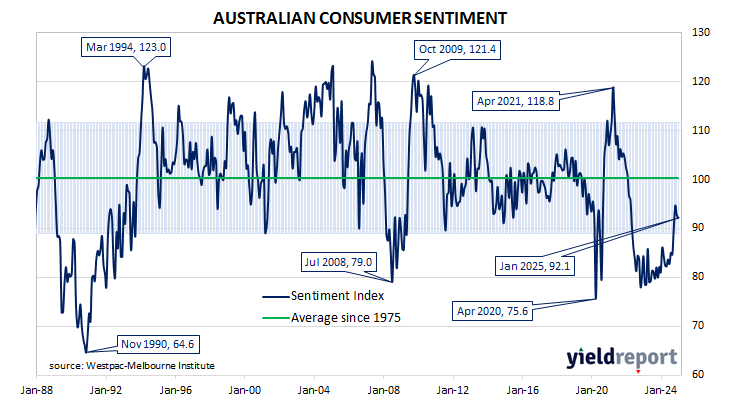

Summary: Westpac-Melbourne Institute consumer sentiment index declines in January; Westpac: the two sub-indexes tracking current conditions decline, forward-looking ones either flat or increasing; ACGB yields decline; rate-cut expectations firm; Westpac: possible consumers reacting to news about AUD depreciation; just one of five sub-indices falls; more respondents expecting higher jobless rate.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment then weakened considerably and languished at pessimistic levels from mid-2022 while business sentiment generally remained at more robust levels.

According to the latest Westpac-Melbourne Institute survey conducted in the early part of January, household sentiment has deteriorated moderately and is at a level which is somewhat on the pessimistic side. Their Consumer Sentiment Index declined from December’s reading of 92.8 to 92.1, a reading which is noticeably lower than the long-term average reading of just over 101.

“In January, the two sub-indexes tracking current conditions declined while the forward-looking ones were flat or increasing, a reversal of the pattern in December,” said Westpac chief economist Luci Ellis.

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

Commonwealth Government bond yields declined modestly across the curve on the day. By the close of business, 3-year and 10-year ACGB yields had both lost 2bps to 4.04% and 4.65% respectively while the 20-year yield finished 1bp lower at 5.03%.

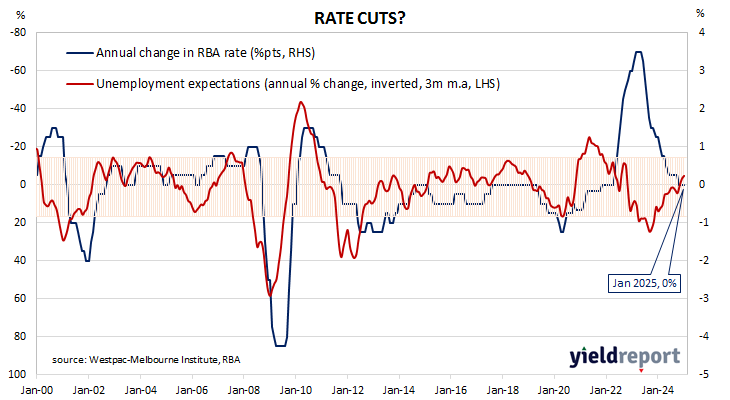

Expectations regarding rate cuts in the next twelve months firmed, with a February cut now viewed as a good chance. Cash futures contracts implied an average of 4.27% in February, 4.03% in May and 3.85% in August. December contracts implied 3.72%, 62bps less than the current cash rate.

“As well as the ongoing unsettled global backdrop, it is possible that consumers were reacting to news about the depreciation of the Australian dollar against the US dollar, which resulted in some negative headlines about the outlook for interest rates and the broader economy,” Ellis added.

Only one of the five sub-indices registered a lower reading, with the “Family finances versus a year ago” sub-index again posting the sole monthly loss.

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 123.7 to 127.2, slightly below the long-term average of 129.1. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.