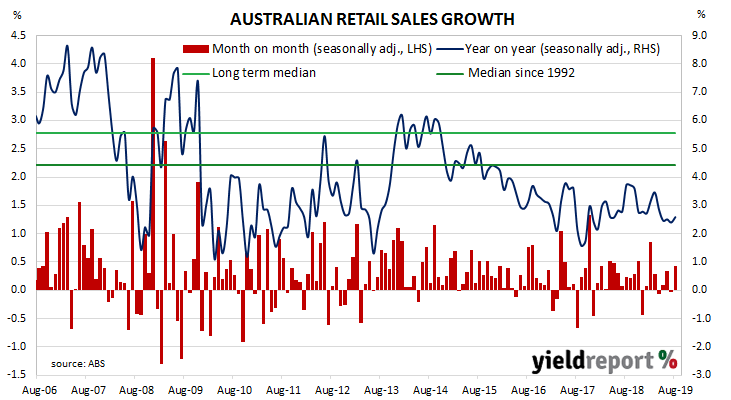

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered a growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018. 2019 has produced a number of low-growth months along with the odd surprisingly strong result, lowering the annual growth rate. The latest figures are largely in line with this pattern.

According to the latest ABS figures, total retail sales increased by +0.4% in August on a seasonally-adjusted basis, a little less than the +0.5% increase which had been expected but an improvement from July’s flat result. On an annual basis, retail sales increased by 2.6%, up from July’s comparable figure of 2.4%.

Westpac senior economist Matthew Hassan said, “While this was broadly in line with the consensus forecast of a 0.5% gain, it is a disappointing result given the scale of the policy stimulus boost to disposable incomes.”

US Treasury yields had fallen heavily overnight, especially those of 2-year bonds. Local bond yields fell on the day but not as much as their US counterparts. By the end of the day, the yield on 3-year ACGBs had slipped 1bp to 0.57%, the 10-year rate had fallen by 3bps to 0.89% and 20-year yields had shed 5bps to 1.30%.

US Treasury yields had fallen heavily overnight, especially those of 2-year bonds. Local bond yields fell on the day but not as much as their US counterparts. By the end of the day, the yield on 3-year ACGBs had slipped 1bp to 0.57%, the 10-year rate had fallen by 3bps to 0.89% and 20-year yields had shed 5bps to 1.30%.

In the cash futures market, the implied probability of a 25bps cut at the RBA’s November meeting remained at 48% while February contracts continued to fully factor in a rate cut which would take the cash rate target down to 0.50%. End of day prices of May 2020 contracts implied a 57% chance of a 0.25% cash rate, up from the previous day’s 55%.