Summary: Leading index growth rate down in August; Westpac: momentum improved relative to 2022, 2023, but still soft; reading implies annual GDP growth of around 2.25%-2.50%; ACGB yields rise; rate-cut expectations soften; Westpac: expects extended period of sluggish performance to last even longer; Westpac: forecasts 1% GDP growth in calendar 2024, 2.4% in calendar 2025.

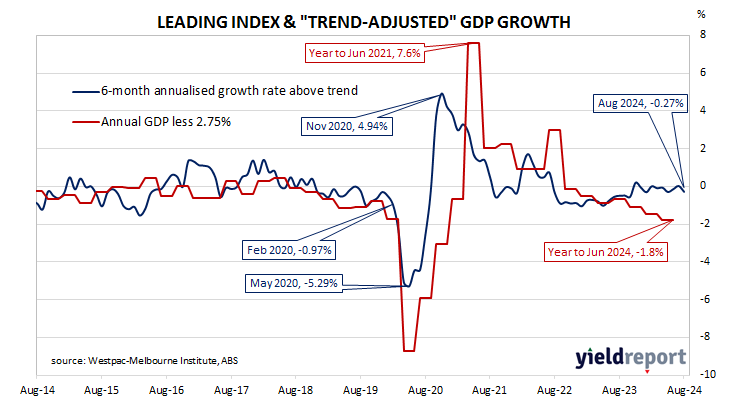

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings spiked towards the end of 2020 but then trended lower through 2021 and 2022 before flattening out in 2023 and 2024.

August’s reading has now been released and the six month annualised growth rate of the indicator registered -0.27%, down from July’s revised figure of +0.04%. The index reading represents a rate relative to “trend” GDP growth, which is generally thought to be around 2.50% to 2.75% per annum in Australia.

“The fall takes the Index growth rate to an eight-month low, albeit still in the –0.3% to +0.2% range that has prevailed since November last year,” said Westpac senior economist Matthew Hassan. “Momentum has improved relative to 2022 and 2023 but is still soft.”

Westpac states the index leads GDP growth by “three to nine months into the future” but the highest correlation between the index and actual GDP figures occurs with a three-month lead. The current reading may therefore be considered to be indicative of an annual GDP growth rate of around 2.25% to 2.50% in the next quarter.

Domestic Treasury bond yields moved moderately higher across the curve.on the day. By the close of business, 3-year, 10-year and 20-year ACGB yields had all gained 3bps to 3.36%, 3.88% and 4.26% respectively.

Expectations regarding rate cuts in the next twelve months softened a little, albeit with a February 2025 rate cut still fully priced in. Cash futures contracts implied an average of 4.325% in September, 4.325% in October, 4.26% in November and 4.035% in February 2025. August 2025 contracts implied 3.315%, 102bps less than the current cash rate.

“Westpac expects this extended period of sluggish performance to last even longer,” Hassan added. “GDP growth is forecast to lift from 1% currently to 2.4% in 2025, an improvement but consistent with the sub-trend signal from the Leading Index.”

The RBA’s August Statement on Monetary Policy forecasts are somewhat higher than Westpac’s latest numbers. The RBA forecasts GDP growth for the years ending December 2024 and December 2025 to be 1.7% and 2.3% respectively.