Unlike the weeks prior to recent CPI reports, the level of attention given to this latest CPI report has been relatively scant. The latest RBA board meeting minutes indicate Australia’s central bank is focussed on the employment market and risks in the housing markets (Sydney and Melbourne). Mentions of underlying inflation were mostly limited to stating how any rise was expected to be gradual. While some commentators noted the importance of the upcoming CPI report, other issues, such as Trump’s tax plans, tended to divert attention away from it.

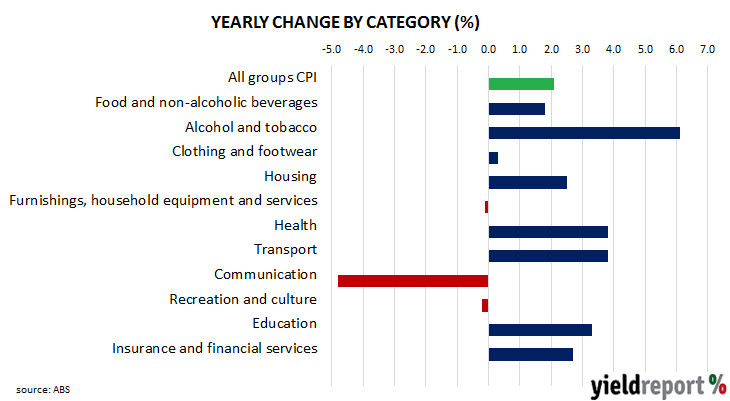

The figures have now been released by the ABS and they were weaker than the market expected, for all three inflation measures (headline, seasonally-adjusted and core). Both headline and seasonally-adjusted inflation came in at 0.5% and 2.1% for the year, each 0.1% under market expectations.

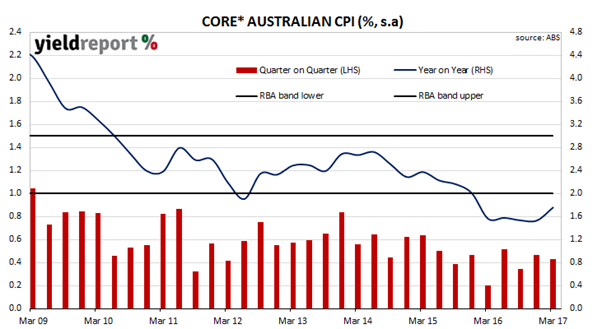

“Core” inflation measures favoured by the RBA, such as the “trimmed mean” and the “weighted median”, were slightly below consensus when considered together. For the quarter, both the trimmed-mean and weighted-median measures increased by 0.4% and the average of the two annual rates came in at 1.8%. Market expectations were for 0.5% for the quarter and 1.9% for the year.

Bond yields went higher on the day. 3 year yields were up 3bps at 1.88% and 10 year bond yields finished the day 4bps higher at 2.66%. The AUD dropped immediately from 75.45 US cents to 75.20 US cents and then fell further during the evening. A weaker currency with higher bond yields seems to be at odds until one realises the Australian bond market was also reacting to two days of higher yields in offshore markets after the ANZAC Day holiday.