Summary: Private sector credit flat after three months of falls; steady growth in owner-occupier segment offset by falls in business loans, personal debt; business credit expected to decline “for some time”; “struggling” housing credit linked to “fragile” jobs market.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April.

According to the latest RBA figures, private sector credit remained unchanged in August following three consecutive months of contraction. The result was slightly above the -0.1% which had been generally expected and above July’s -0.1%. However, the annual growth rate slowed to 2.2% from July’s comparable rate of 2.4%.

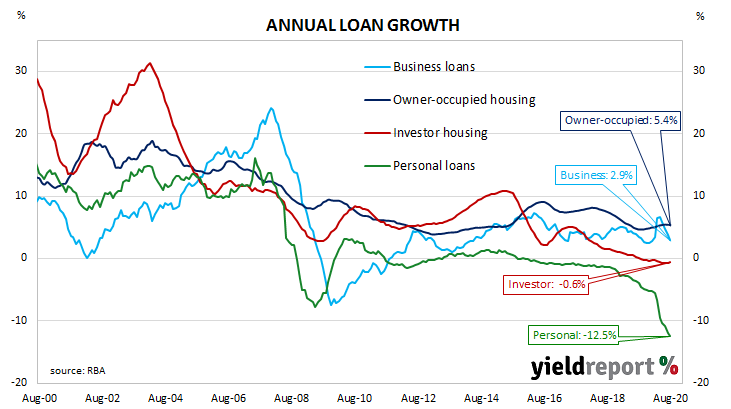

Owner-occupier loans continued to grow steadily but their growth was offset by falls in business loans and personal debt.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to favour a slight easing. At the end of the day, contract prices implied the cash rate would trade in a range between 0.065% and 0.085% through to the end of 2021.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.4% over the month, the same rate as in the previous three months. The sector’s 12-month growth rate remained at 5.4%.

Growth rates in the business sector had been slowing until they picked up in the first quarter, with an especially large increase in March which was followed by a small increase in April. The slowdown restarted in May and it has continued through to August as business credit contracted by 0.4%, a little higher than the 0.6% fall in July. The segment’s annual growth rate slowed from July’s rate of 3.7% to 2.9%.