Last week YieldReport reported on the RBA’s Guy Debelle comments to the Actuaries Institute Seminar in Sydney.

At the same seminar, APRA’s chair, Wayne Byres, gave a speech that implied some changes were coming which would ultimately lead to higher term deposit rates.

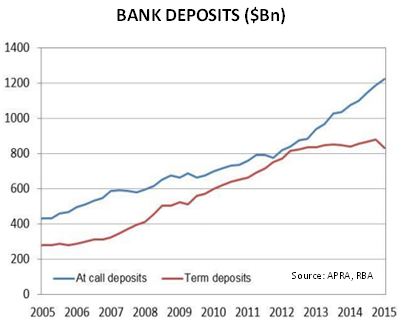

This is good news for term deposit holders that have seen TD rates slashed in the past 12 months and that have struggled to find alternative secure investments paying a reasonable yield in the face of extreme market volatility.

Wayne Byres told traders and investors that banks would need to change their balance sheets to prepare for new liquidity rules due in 2018. The APRA chairman said banks and other approved deposit-taking institutions still faced liquidity risks in spite of changes made to funding since the GFC. He also said overall leverage ratios had not really improved.

ADIs had pursued deposit growth to replace borrowing on short-term wholesale markets but the deposit growth has primarily come in the form of at-call deposits rather than term deposits. UBS said in a research note “Over the last three years the banks have been actively reducing their term deposit rates to help alleviate margin pressure.” At call deposits are less “sticky” than term deposits in the sense that depositors have easier access to them and could flee quickly in the event of a banking crisis. Post-GFC banks were fiercely competitive for term deposits, paying string premiums above the standard or ‘blackboard’ rate. Mr Byres said the lessening of competition for deposits, what he referred to as the “ceasefire” among banks when it came to competing for customers’ deposits, meant “liquidity profiles had been strengthened less than it might first appear.”

He went on to say ADIs had not materially reduced their reliance on offshore short-term wholesale funding which was typical of funding which was most likely to disappear in a crisis. As a percentage of total funding, this type of funding was “virtually unchanged” over the last ten years. “The largest Australian banks do not easily meet the new (“net stable funding ratio” due in 2018) standard” and further lengthening of Australian banks’ maturity profiles was probably required to “truly strengthen their funding resilience.”

As UBS put it: “APRA would like to see more term deposit funding … in our view the only way banks could achieve this is via higher term deposit interest rates.”