Summary: Home approval numbers up 18.5% in December, above expectations; 3.8% lower than December 2021; ANZ: still on downward trend; house approvals down 2.4%, apartments up 58.8%; non-residential approvals down 1.7% in dollar terms, residential alterations down 3.0%.

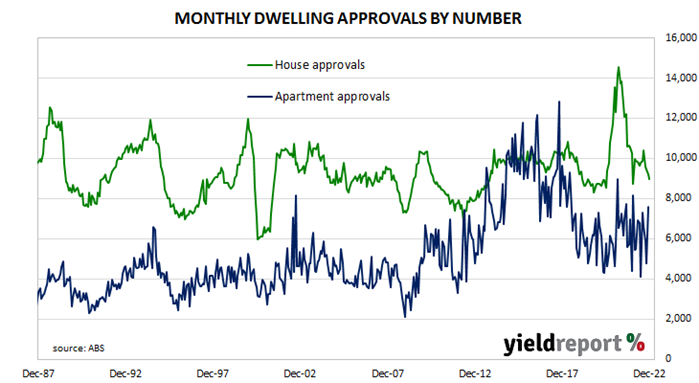

Building approvals for dwellings, that is apartments and houses, headed south after mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and the early months of 2020 painted a picture of a recovery taking place, even as late as April of that year. Subsequent months’ figures then trended sharply upwards before falling back in 2021 and 2022.

The Australian Bureau of Statistics has released the latest figures from December which show total residential approvals rose by 18.5% on a seasonally-adjusted basis. The increase was considerably more than the 1.0% rise which had been generally expected and it contrasted with November’s -8.8%. However, total approvals still fell by 3.8% on an annual basis, up from the previous month’s figure of -14.1%. Monthly growth rates are often volatile.

“So, despite the strong monthly result, we still think approvals are likely on a downward trend,” ANZ senior economist Adelaide Timbrell. “While Australia’s strong expected net migration through this year will limit the total decline in building approvals, falling home prices and rising rates will reduce appetite for new dwelling developments.”

Commonwealth Government bond yields fell moderately on the day with the exception of ultra-long yields which did not move. By the close of business, the 3-year ACGB yield had lost 6bps to 3.15%, the 10-year yield had shed 3bps to 3.55% while the 20-year yield finished unchanged at 3.96%.

In the cash futures market, expectations regarding future rate rises firmed a touch. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.06% to average 3.24% in February and then increase to an average of 3.41% in March. May 2023 contracts implied a 3.63% average cash rate while August 2023 contracts implied 3.72%.

Approvals for new houses fell by 2.4% over the month, the same percentage fall as in November. On a 12-month basis, house approvals were 12.2% lower than they were in December 2021, up from November’s comparable figure of -12.8%.

Apartment approval figures are usually a lot more volatile and December’s total jumped by 58.8% after a 19.1% fall in November. The 12-month growth rate rose from November’s revised rate of -16.5% to 8.7%.

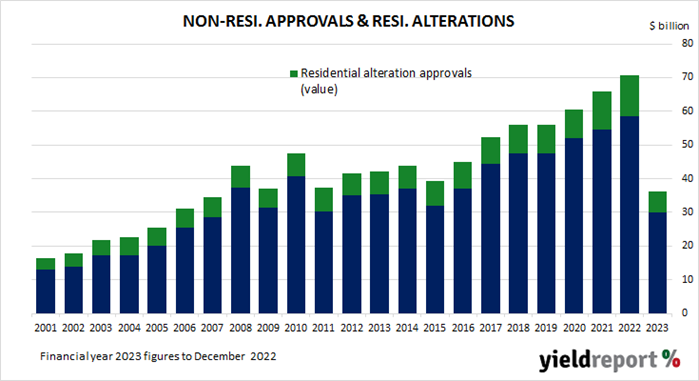

Non-residential approvals declined by 1.7% in dollar terms over the month but were still 16.3% higher on an annual basis. Figures in this segment also tend to be rather volatile.

Residential alteration approvals decreased by 3.0% in dollar terms over the month but were 0.3% higher than in December 2021.