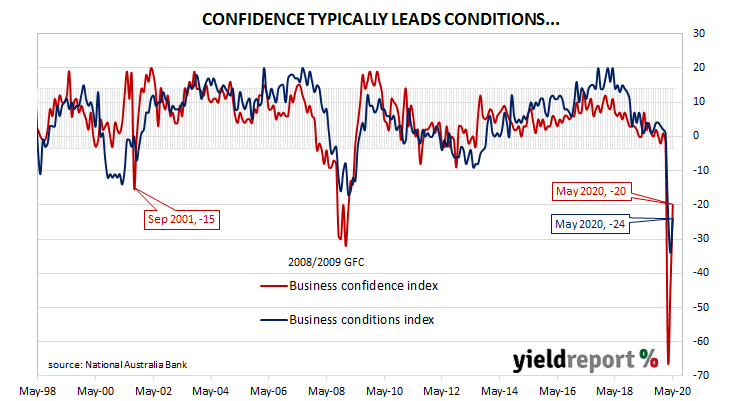

Summary: Business confidence improved for the second consecutive month; conditions up, back to March’s level; capacity usage recovers; capex responses imply expansion plans restrained; confidence currently on par with 1990s recession.

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s conditions index then began to slip and, by the end of 2018, they had dropped to below-average levels. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and NAB’s business confidence index began trending lower, with the conditions index following. In March 2020, vastly lower readings began to reflect coronavirus containment measures.

According to NAB’s latest monthly business survey of 400 firms conducted in the latter part of May, business conditions recovered from most of April’s deterioration. NAB’s conditions index registered -24, up from April’s reading of -34.

NAB chief economist Alan Oster said, “Business conditions saw a broad-based improvement in the month but remain deeply negative, at a level last seen coming out of the GFC.” However, he also noted “all industries continue to expect a deterioration in conditions.” Westpac senior economist Andrew Hanlan appeared more optimistic. “Clearly the situation remains fluid and fast moving. The continued easing of restrictions in June will see a further bounce in business conditions.”

Business confidence moved higher for a second consecutive month. NAB’s confidence index rose from April’s revised reading of -45 to -20. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time. NAB’s Oster said confidence “increased further from its low point in March, but remains weak with a current reading last seen around the trough in the 1990s recession.” The figures came out on the same day as ANZ’s latest Job Ads series and Commonwealth bond yields moved lower, although they may have only followed US Treasury movements to some degree. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.28%, the 10-year yield had lost 7bps to 1.09% while the 20-year yield finished 4bps lower at 1.69%.

The figures came out on the same day as ANZ’s latest Job Ads series and Commonwealth bond yields moved lower, although they may have only followed US Treasury movements to some degree. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.28%, the 10-year yield had lost 7bps to 1.09% while the 20-year yield finished 4bps lower at 1.69%.

In the cash futures market, expectations of a rate cut barely changed. By the end of the day, July contracts implied a rate cut down to zero as a 54% chance, unchanged from the previous day. August contracts implied a 46% chance of such a move in that month, also unchanged. Contract prices of months in the remainder of 2020 and through to late-2021 implied similar probabilities, ranging between 33% and 47%.