Summary: Business conditions deteriorate for second month; confidence recovers chunk of December loss; infections trigger consumer caution, staff shortages; firms optimistic outbreak will be short-lived; ANZ data points to recovery in conditions, confidence “will likely grow”; capacity utilisation rate up; 6 of 8 sectors of economy at/above respective long-run averages; inflationary pressures continue.

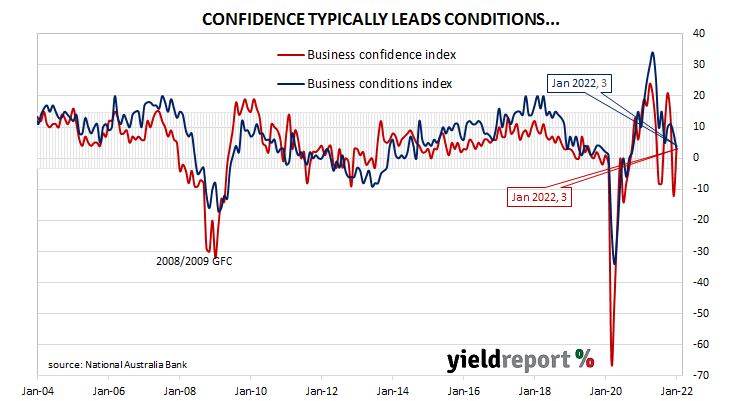

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip, declining to below-average levels by the end of 2018. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and the index trended lower, hitting a nadir in April 2020 as pandemic restrictions were introduced. Conditions improved markedly over the next twelve months, only to revert back to more normal levels in the latter part of 2021.

According to NAB’s latest monthly business survey of over 400 firms conducted over the last two weeks of January, business conditions have deteriorated for a second month. NAB’s conditions index registered 3, down from December’s reading of 8.

NAB senior economist Brody Viney said the latest wave of coronavirus infections had “triggered consumer caution and staff shortages” He noted NAB’s indices which track firms’ profitability, trading conditions and employment, all fell.

In contrast, business confidence recovered a good chunk of what was lost in December. NAB’s confidence index rose from December’s reading of -12 to +3, just a few points below the long-term average. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

“The confidence rebound signals that, despite the disruption, firms were optimistic that the outbreak would be short-lived and, consistent with this, forward order remain steady,” Viney added

Commonwealth Government bond yields increased markedly on the day. By the close of business, the 3-year ACGB yield had gained 8bps to 1.60% while 10-year and 20-year yields both finished 13bps higher at 2.14% and 2.61% respectively.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.05%, firmed a little in favour of rate rises in the second half of 2022. At the end of the day, contract prices implied the cash rate would rise gradually from the current rate of 0.050% to 0.155% by May, then increase to 0.575% by August and then to 1.395% by February 2023.

ANZ senior economist Adelaide Timbrell said some of her bank’s other economic reports point to a recovery of conditions. “We expect a quick bounce back in February, with both ANZ-Roy Morgan Australian Consumer Confidence and ANZ spending data improving in late January.” She also noted business confidence “will likely grow as the Omicron wave passes its peak.”

NAB’s measure of national capacity utilisation partially recovered from December’s revised figure of 80.7% to 81.6%. Six of the eight sectors of the economy were reported to be operating at or above their respective long-run averages. The retail and recreational/personal services sectors were the exceptions.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.

As with December’s report, there were several references to inflationary pressures. “Cost pressures remained elevated, with purchase cost growth reaching a record 3.4% in quarterly terms. Strong wage bill growth continued while on the output side, final product price inflation remained elevated, although retail price inflation eased somewhat.”