Summary: Business conditions improve in January; confidence also improves; trading conditions, profitability, employment sub-indices all stronger, well above average; talk of slowdown possibly “premature”; demand “elevated”, supported by strong population growth, easing concerns regarding global growth prospects; capacity utilisation rate higher, remains elevated.

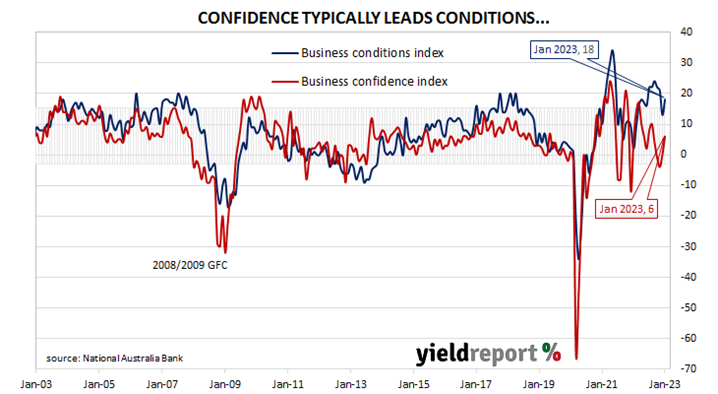

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 as the index trended lower. It hit a nadir in April 2020 as pandemic restrictions were introduced but then conditions improved markedly over the next twelve months. Subsequent readings were generally in a historically-normal range until the second half of 2022.

According to NAB’s latest monthly business survey of over 400 firms conducted in last few days of January, business conditions have improved after deteriorating in the previous three months. NAB’s conditions index registered 18 points, up 5 points from December’s revised reading.

Similarly, business confidence also improved. NAB’s confidence index increased from December’s revised reading of 0 points to 6 points, in line with the long-term average. Typically, NAB’s confidence index leads the conditions index by one month, although some divergences have appeared from time to time.

“The rise was led by very strong trading conditions in the month but both profitability and employment are also well above average,” said NAB senior economist Brodey Viney.

Commonwealth Government bond yields moved lower on the day. By the close of business, the 3-year ACGB yield had slipped 1bp to 3.47%, the 10-year yield had lost 2bps to 3.75% while the 20-year yield finished 3bps lower at 4.08%.

In the cash futures market, expectations regarding future rate rises over the next few months softened a little. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.32% to average 3.495% in March and then increase to an average of 3.895% in May. August contracts implied a 4.11% average cash while November contracts implied 4.095%.

”Talk of a slowdown in the business sector may have been a little premature,” said ANZ economist Madeline Dunk. “Some of the improvement in today’s numbers could reflect a correction from last month’s report, where many of the survey’s indicators recorded annual lows.”

“Overall, the survey suggests the economy has remained resilient to headwinds from inflation and higher interest rates,” Viney added. “Demand has remained elevated, likely supported by strong population growth, and concerns about global growth prospects appear to have eased.”

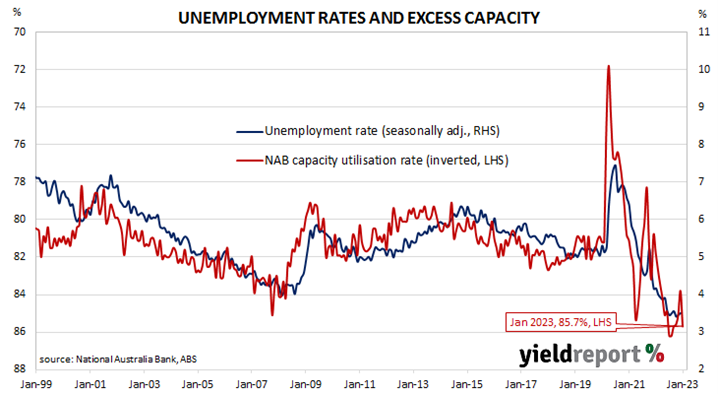

NAB’s measure of national capacity utilisation remained at a historically-elevated level as it increased from December’s revised figure of 83.8% to 85.7%. All eight sectors of the economy were reported to be operating above their respective long-run averages.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.