Summary: Business conditions deteriorate in May, remain at elevated level; confidence also deteriorates, back to long-term average; most businesses in strong position despite inflation headwinds, yet to feel effects of higher rates, global growth risks; businesses now facing series of future hikes, likely to have muted confidence; activity conditions are robust, consumers have money on hand to spend more freely; capacity utilisation rate up, all 8 sectors of economy above respective long-run averages.

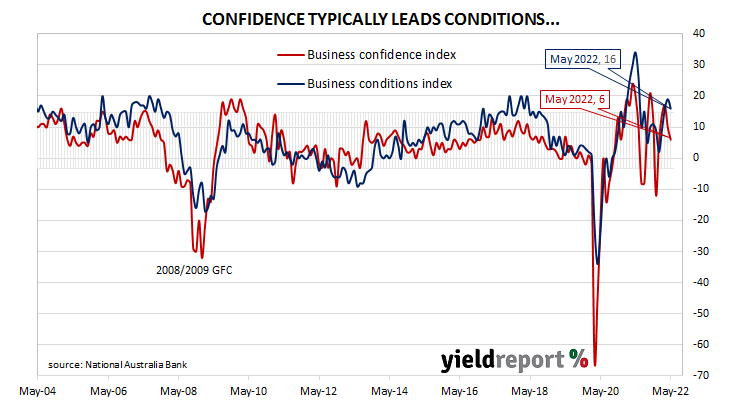

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 as the index trended lower. It hit a nadir in April 2020 as pandemic restrictions were introduced but then conditions improved markedly over the next twelve months. Readings have been generally in a historically-normal range since then.

According to NAB’s latest monthly business survey of over 550 firms conducted over the last week of May, business conditions have deteriorated somewhat but remain at an elevated level. NAB’s conditions index registered 16, down from April’s revised reading of 19.

Business confidence also deteriorated. NAB’s confidence index fell from April’s reading of 10 to 6, thus reverting back to the long-term average. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

“Overall, the survey indicates the economy has maintained its momentum in Q2 and most businesses are in a strong position despite the inflation headwinds, with the lift-off in official interest rates and global growth risks yet to significantly impact Australia’s economic trajectory,” said NAB senior economist Brody Viney.

Commonwealth Government bond yields rocketed up on the day. By the close of business, the 3-year ACGB yield had gained 21bps to 3.48% while 10-year and 20-year yields both finished 18bps higher at 3.96% and 4.15% respectively.

In the cash futures market, expectations of a steeper path for the actual cash rate over time hardened. At the end of the day, contracts implied the cash rate would rise from the current rate of 0.81% to 1.275% in July and then increase to 1.86% by August. November contracts implied a 3.30% cash rate while May 2023 contracts implied 4.18%.

“The results were a bit of a mixed bag and there were a number of influences at play,” said ANZ economist Madeline Dunk. “The survey period was just after the federal election and also captured sentiment following the RBA’s first rate hike in 11 years in early May. Businesses are now facing a series of future hikes and this is likely to have muted confidence.”

Westpac senior economist Andrew Hanlan noted conditions facing the business sector are still good. “The key theme remains that activity conditions are robust currently, with a reopening bounce from the delta lockdowns and the omicron wave disruptions. Fewer COVID related restrictions give consumers more opportunities to spend and, in general, they have the money on hand to spend more freely.”

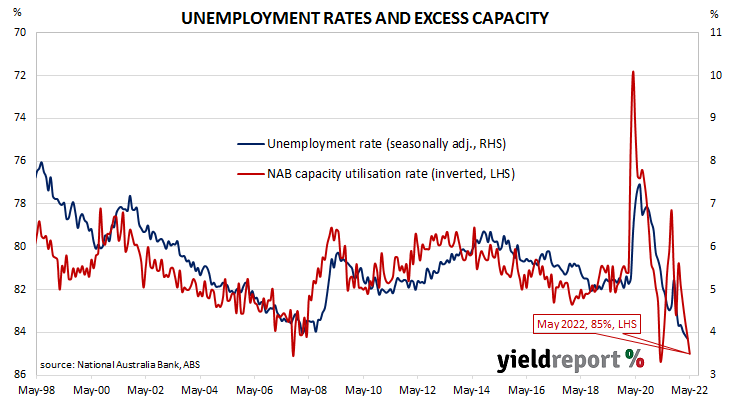

NAB’s measure of national capacity utilisation continued to recover from December’s drop and it rose from April’s revised figure of 84.2% to 85.0%. All eight sectors of the economy were reported to be operating above their respective long-run averages.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.