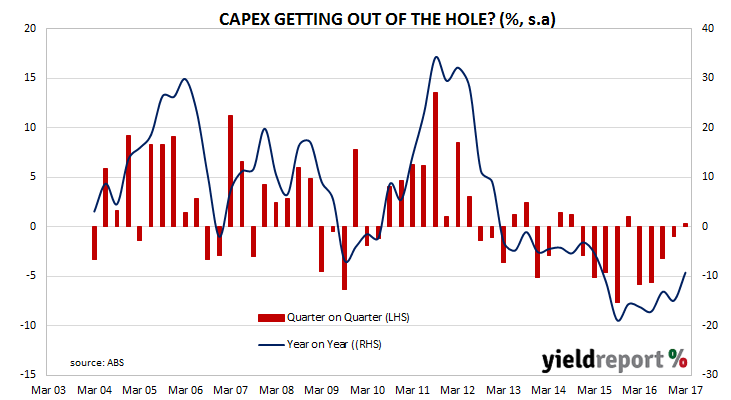

First quarter private capital expenditure (capex) figures have now been released by the ABS and the +0.3% quarter-on-quarter figure was in line with market expectations. Year on year, capex was 9.3% lower, as mining investment falls back to more normal levels after the mining investment spike of 2011/2012.

The Aussie dropped by about 0.25 US cents immediately after the figures were released and then finished another 0.25 cents lower at around 73.75 U.S. cents. Both 3 year and 10 year bond yields had edged up 1bps to 1.68% and 2.43% respectively but retail sales figures were released simultaneously and thus the markets’ reactions to either report is somewhat clouded.

The reception the figures received was on a scale ranging from vaguely positive to quite negative. NAB economist Tapas Strickland had one of the more negative views. “The non-mining investment outlook for 2017/18 failed to lift further, while flat equipment investment in the quarter presents downside risks to Q1 GDP…The lack of a lift in the non-mining components of the survey will be discouraging for the RBA, which has been patiently awaiting a lift in non-mining investment intentions in the data.” The team at ANZ Research shared his sentiment. “Importantly, spending on plant and equipment, which feeds into next week’s Q1 GDP, fell 0.1%. This is much softer than our expectation of moderate growth. As such it poses downside risk to our already soft pick for Q1 GDP.”

CBA senior economist Gareth Aird provided one of the few (slightly) positive views out there. “The NAB Business Survey continues to suggest a lift in investment is forthcoming. But we think the softness in consumer demand is holding investment back. Fortunately there is a decent amount of public capex to come because the outlook for private investment remains weak.”