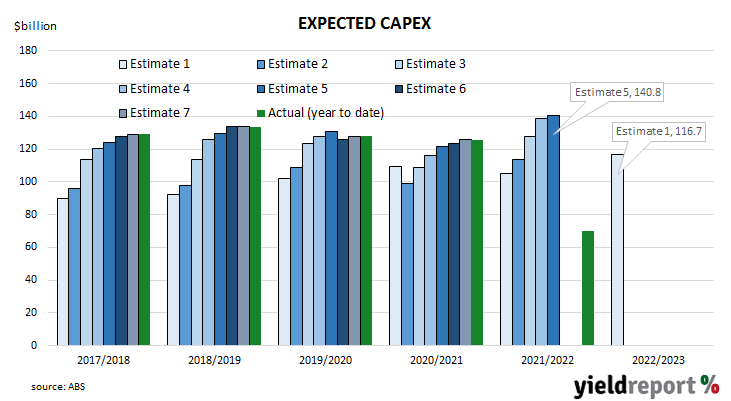

Summary: Private capital expenditures up 1.1% in December quarter; less than 2.5% expected; reflects capacity constraints, supply-chain disruptions; 2021/22 capex estimate 1.2% higher than November’s estimate, 16.0% higher than comparable estimate from 2020/21; 2021/22 capex expectations not as strong as expected, usual upgrades occur earlier.

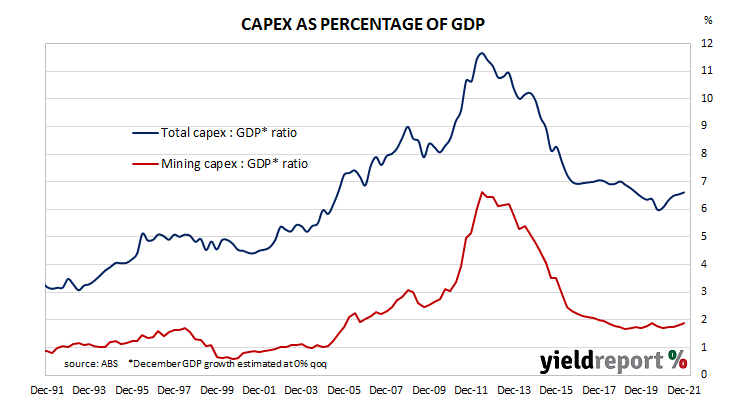

Australia’s private capital expenditure (capex) spiked early in the 2010s on the back of investment in the mining sector. As projects were completed, capex growth rates fell away and generally remained negative for a good part of a decade. Capex as a percentage of GDP is now back to a level more in line with the 30-year average.

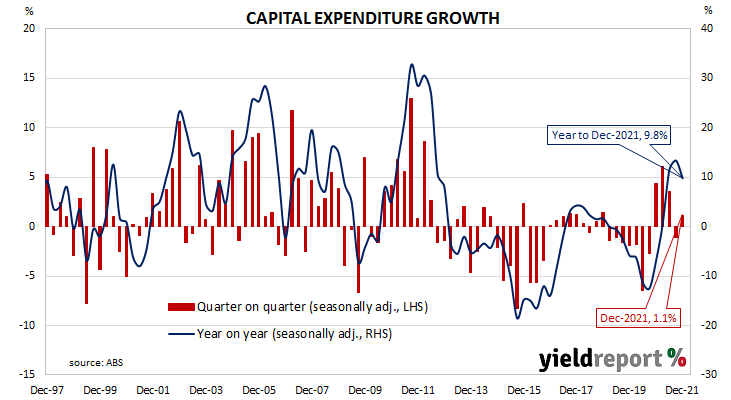

According to the latest ABS figures, seasonally-adjusted private sector capex in the December quarter increased by 1.1%. The result was less the 2.5% rise which had been expected but in contrast to the September’s revised figure of -1.1%. On a year-on-year basis, total capex increased by 9.8% after recording an annual rate of +13.4% in the previous quarter.

NAB economist Taylor Nugent said the lower-than-expected result “are more likely to be a reflection of capacity constraints and supply-chain disruptions rather than a negative signal for the demand outlook.”

Commonwealth Government bond yields dropped on the day as investors fled equity markets on news of Russia’s invasion of Ukraine. By the close of business, the 3-year Treasury bond yield had shed 9bps to 1.66% while 10-year and 20-year yields each finished 11bps lower at 2.17% and 2.61%.

Expectations of the cash rate’s path over time were pulled lower in the cash futures market. At the end of the day, contract prices implied the cash rate would not exceed the RBA’s 0.10% target rate until May and then rise to 0.47% by August. February 2023 contracts implied a cash rate of 1.355%.

The report also contains capex estimates for the current financial year. The latest capex estimate for the 2021/22 financial year, Estimate 5, is $140.8 billion, 1.7% higher than November’s Estimate 4 and 16.0% higher than Estimate 5 of the 2020/21 financial year.

“Expectations for 2021/22 capex were not as strong as we expected in Q4, after a very strong upgrade in Q3, said ANZ senior economist Adelaide Timbrell. “When we look at the difference between Q2 expectations and Q4, the six-month change is close to the average for the previous five years. So rather than firms getting shaky about Omicron, we think it’s more likely that their usual upgrade in expectations occurred earlier than usual.”