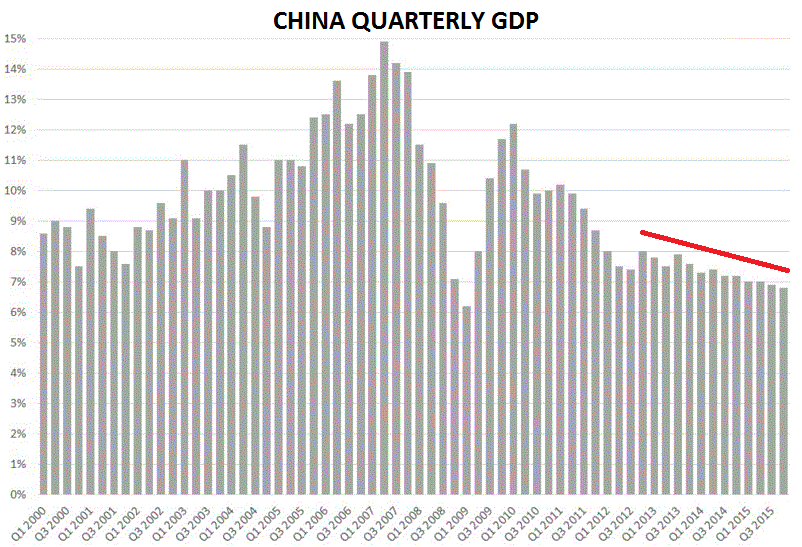

China’s National Bureau of Statistics released Q4 2015 GDP figures that indicated a quarterly increase of 1.6%, 0.2% lower than market expectations. The annual growth rate was 6.8% and slightly lower than the expected 6.9%. It was the lowest growth level in 25 years.

That, of course, is if you believe the numbers. There is a fair degree of scepticism regarding the validity of Chinese economic data and a look at the quarterly GDP figures from the start of 2014 indicates some of the reasons for suspicion. Given the volatility in the GDP data prior to 2014, the smooth decline of GDP figures afterward is either a remarkable fluke, a display of unprecedented economic policy skill or “data smoothing”.

Nonetheless, the release of the GDP numbers saw local bond market 10 year yields initially move up a point to 2.65% but then fall away to 2.61%. In the foreign exchange market the AUD sold off by US 0.5 cent before recovering back to close to the pre-announcement level.

China’s transition from a reliance on exports to domestic consumption and service provision needs more time and government support according to AMP Capital’s Shane Oliver. “Growth is still soft but it’s not collapsing…policy stimulus measures are helping but more is needed.”

Three months ago, Westpac focussed on the nominal GDP figure which the bank sees as a more reliable gauge of underlying demand conditions. This time the bank said, “Overall, the loss of momentum evident in the nominal series is a disappointing result…in through the year terms, that (the latest data) equates to a 5.8%yr pace in Q4, from 6.2% in Q3 and 7.1%.”