Summary: Conference Board leading index up 0.3% in March; in line with expectations; signals economic growth “likely to continue through 2022”; still forecasts 3.0% US GDP growth for calendar 2022 but “downside risks” remain.

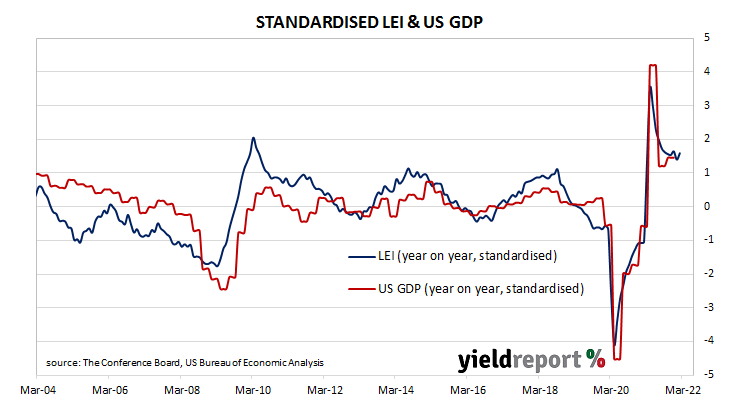

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April of 2020 signalled “a deep US recession” while subsequent readings indicated the US economy would recover rapidly.

The latest reading of the LEI indicates it increased by 0.3% in March. The result was in line with the consensus forecast but half of February’s revised figure of 0.6%. On an annual basis, the LEI growth rate slowed from 9.3% after revisions to 8.1%.

“The US LEI rose again in March despite headwinds from the war in Ukraine,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board. “This broad-based improvement signals economic growth is likely to continue through 2022 despite volatile stock prices and weakening business and consumer expectations.

US Treasury bond yields rose on the day, especially at the front of the curve. By the close of business, the 2-year yield had jumped 11bps to 2.67%, the 10-year yield had gained 7bps to 2.91% while the 30-year yield finished 5bps higher at 2.93%.

In terms of US Fed policy, expectations of a higher federal funds range over the next 12 months hardened considerably. May contracts implied an effective federal funds rate of 0.785%, 34bps higher than the current spot rate. June contracts implied a rate of 1.12% while March 2023 futures contracts implied an effective federal funds rate of 3.02%, 269bps above the spot rate.

The Conference Board is still expecting US GDP growth of 3.0% over calendar-year 2022, with a 0.5 percentage point discount factored in for the war in Ukraine. However, Ozyildirim noted “downside risks” remain, pointing to further supply-chain disruptions, shutdowns, tightening monetary policy and labour shortages.

Regression analysis suggests the latest reading implies a 4.3% year-on-year growth rate in June, down from May’s revised figure of 4.8%.