Summary: US leading index up 0.9% in July, above expectations; “consistent with strong economic growth” in second half; Delta variant, rising inflation fears “could create headwinds” in near term. Conference Board 2021 forecast revised down from 6.6% to 6.0%.

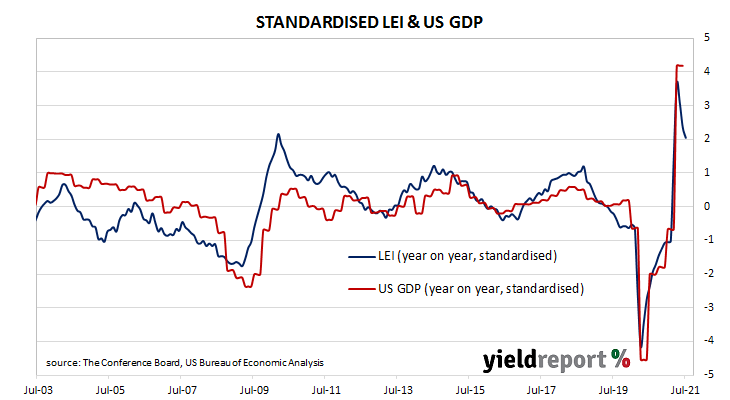

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April of 2020 signalled “a deep US recession” while subsequent readings indicated the US economy had recovered rapidly.

The latest reading of the LEI indicates it rose by 0.9% in July. The result was above the 0.7% increase which had been generally expected and higher than June’s revised figure of 0.5%. On an annual basis, the LEI growth rate slowed from 11.9% after revisions to 10.7%.

“The Leading Index’s overall upward trend, which started with the end of the pandemic-induced recession in April 2020, is consistent with strong economic growth in the second half of the year,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board. However, he noted “the Delta variant and/or rising inflation fears could create headwinds for the US economy in the near term.”

Changes over time can be large but once they are standardised, a clearer relationship with GDP emerges. The latest reading implies a 5.7% year-on-year growth rate in October, down from September’s comparable figure of 6.3% after revisions. The Conference Board currently forecasts a 6.0% expansion across all of calendar 2021, down from their forecast of 6.6% a month ago.