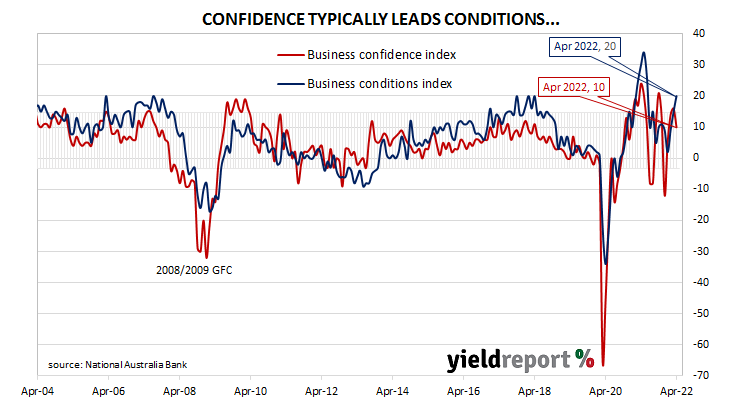

Summary: Business conditions improve in April, at historically-high level; confidence deteriorates, remains above long-term average; confidence, conditions fairly strong across most industries; confidence affected by Federal election, interest rate tightening cycle; capacity utilisation rate up, all 8 sectors of economy at/above respective long-run averages; growth in labour, purchase costs accelerates over past three months, signals “more strong inflation to come”

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 as the index trended lower. It hit a nadir in April 2020 as pandemic restrictions were introduced but then conditions improved markedly over the next twelve months. Readings have been generally in a historically-normal range since then.

According to NAB’s latest monthly business survey of over 400 firms conducted over the last week of April, business conditions have improved to a historically-high level. NAB’s conditions index registered 20, up from March’s revised reading of 15.

In contrast, business confidence deteriorated. NAB’s confidence index fell from March’s reading of 16 to 10, thus remaining above the long-term average. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

“Both confidence and conditions now look fairly strong across most industries, with the exception of transport, utilities and construction where cost pressures have been most acute,” said NAB senior economist Brody Viney.

Short-term Commonwealth Government bond yields fell moderately on the day while longer term yields remained almost steady. By the close of business, the 3-year ACGB yield had shed 5bps to 3.14%, the 10-year yield had returned to its starting point at 3.61% while the 20-year yield finished 1bp higher at 3.91%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.31%, eased slightly. At the end of the day, contract prices implied the cash rate would rise to 0.575% in June and then rise to 1.39% by August. May 2023 contracts implied a cash rate of 3.465%, 315bps above the current cash rate.

“It is understandable that confidence eased somewhat associated with the Federal election which adds to uncertainty around the outlook for public policy. In addition, the beginning of the interest rate tightening cycle is a negative, particularly given the recent aggressive action by the US FOMC,” said Westpac senior economist Andrew Hanlan.

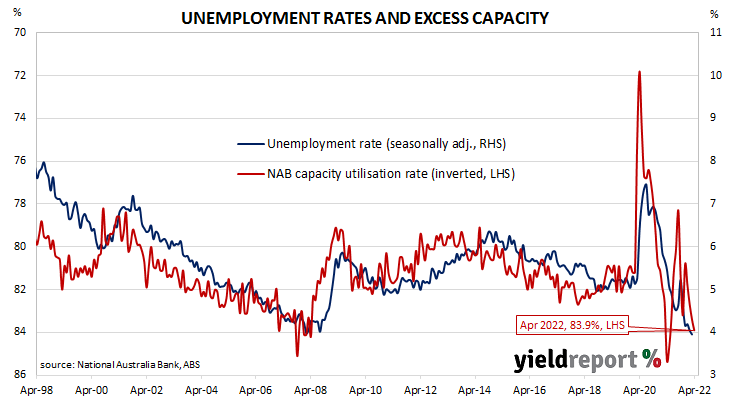

NAB’s measure of national capacity utilisation continued to recover from December’s drop and it rose from March’s revised figure of 83.4% to 83.9%. All eight sectors of the economy were reported to be operating at or above their respective long-run averages.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.

“The growth in both labour costs and purchase costs accelerated in the three months to April, signalling more strong inflation to come, though final product price growth fell a little,” said ANZ senior economist Adelaide Timbrell.