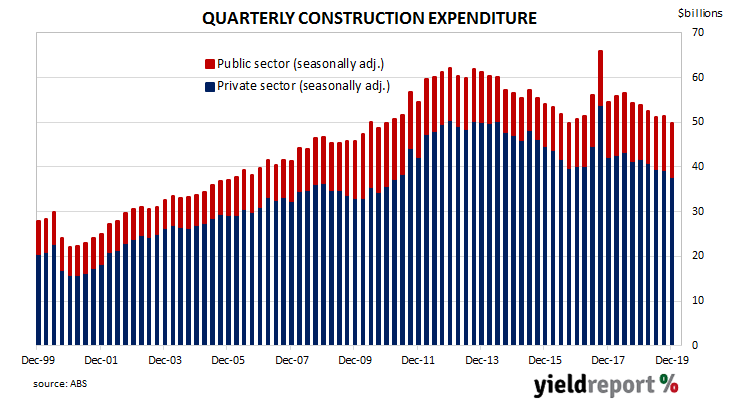

Construction expenditure increased substantially in Australia in the early part of this decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new liquid natural gas projects and the expansion of existing mining projects to exploit a tripling in price of Australia’s mining exports in the previous decade. The return to “normal” investment levels is still continuing.

According to the latest construction figures published by the ABS, the value of construction work has continued the downtrend which began in the September quarter of 2018. Total construction in the December quarter fell by 3.0%, a smaller fall than the 1.0% contraction which had been expected and less than the revised 0.4% increase of the September quarter. On an annual basis, the growth rate deteriorated from September’s revised figure of -5.6% to -7.4%.

ANZ senior economist Catherine Birch said, “The downturn in residential activity accelerated but it was private-sector non-residential construction work done that surprised to the downside. Public sector work done provided a small offset.” Commonwealth Government bond yields finished the day a little lower, somewhat in line with lower US Treasury yields. By the end of the day, the 3-year ACGB yield had lost 3bps to 0.61%, the 10-year yields remained unchanged at 0.92% while the 20-year yield finished 2bps lower at 1.29%.

Commonwealth Government bond yields finished the day a little lower, somewhat in line with lower US Treasury yields. By the end of the day, the 3-year ACGB yield had lost 3bps to 0.61%, the 10-year yields remained unchanged at 0.92% while the 20-year yield finished 2bps lower at 1.29%.

In the cash futures market, traders reacted by hardening their expectations of further official rate cuts in 2020, although a March rate cut was still viewed as quite unlikely. The implied probability of a 25bps cut at the RBA’s March meeting increased from 9% to 11% while April contracts implied a 47% chance of a cut, up from the previous day’s 39%. May 2020 contracts implied another cut in the cash rate target had increased from 69% to 76%. Prices of July contracts continued to have a rate cut fully priced in.