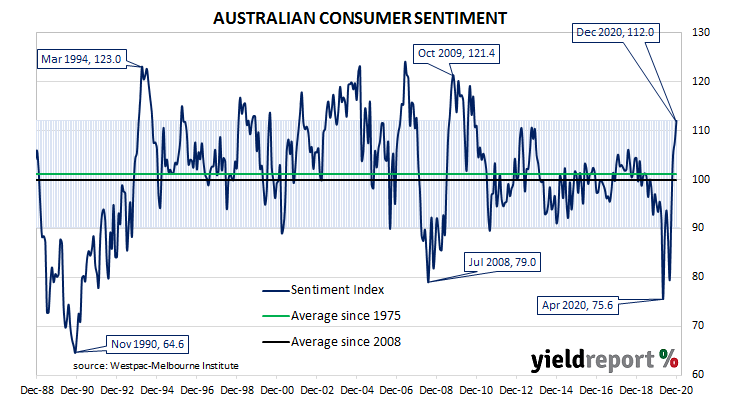

Summary: Household sentiment improves for fourth consecutive month; sentiment “fully recovered” from recession”; index highest since October 2010, substantially above long-term average; all components but one higher; “time to buy a dwelling” index lower.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April but, after a few months of to-ing and fro-ing, it then staged a full recovery.

According to the latest Westpac-Melbourne Institute survey conducted in early December, household sentiment has improved to a reasonably optimistic level. The Consumer Sentiment Index rose for a fourth consecutive month, from November’s reading of 107.7 to 112.0.

“After only eight months the evidence seems clear that sentiment has fully recovered from the COVID recession,” said Westpac chief economist Bill Evans.

Treasury bond yields hardly moved on the day. By the close of business, 3-year and 10-year ACGB yields remained unchanged at 0.19% and 1.02% respectively while the 20-year yield finished 1bp lower at 1.66%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.04%, did not change materially. At the end of the day, contract prices implied the cash rate would trade in a range between 0.04% and 0.05% through to the end of 2021.

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure is the highest since October 2010, substantially above the long-term average reading of just over 101.