Summary: Private sector credit grows at modest rate in April; half expected figure; credit growth “gains momentum”; housing credit growth continues, business loans down, personal loans flat; mortgage pay-downs, weak personal, business credit capping overall rise.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since late-2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April 2020.

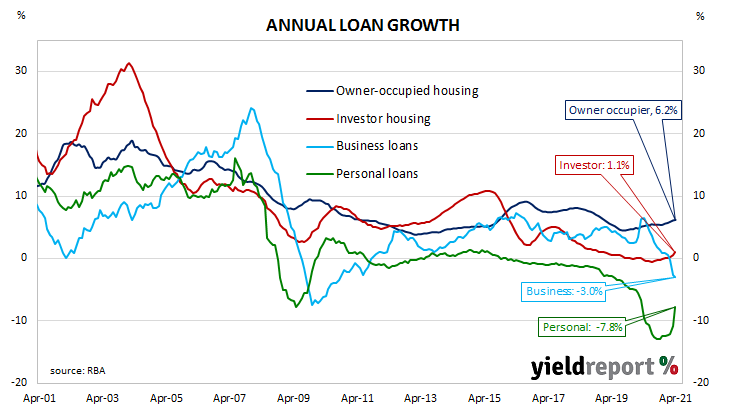

According to the latest RBA figures, private sector credit growth slowed In April, rising by 0.2%. The result was half the generally expected figure of 0.4% and slower than March’s 0.4% increase. However, the annual growth rate still increased from 1.0% in March to 1.3%.

“In 2021, credit growth has gained momentum, with the 3 month annualised pace accelerating to 3.5% in April,” said senior Westpac senior economist Andrew Hanlan.

Owner-occupier loans accounted for about half of the net growth while investor loans accounted for much of the balance. Business loans contracted and personal debt was flat.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.6% over the month, slightly slower than March’s 0.7% increase. The sector’s 12-month growth rate ticked up from 6.1% to 6.2%.

Growth rates in the business sector went into reverse as total business credit contracted by 0.3%, a turnaround from March’s increase of 0.4%. The segment’s annual growth rate remained negative, its contraction rate increasing from March’s revised rate of 2.6% to 3.0%.