For the greater part of the last two decades, inflation rates in advanced economies have been low. Up until around the start of this decade, low inflation had been viewed as a positive. High inflation in the 1970s and early 1980s was thought responsible for distorting investment decisions and it had been accompanied by economic stagnation in western countries. Once the back of inflation had been broken in the U.S in the early 1980s and in Australia in the early 1990s, locking in low inflation rates was a goal of central banks around the world. However, since 2009, central banks in advanced economies have regularly pointed to low inflation rates as a reason for continuing ultra-low interest rate policies.

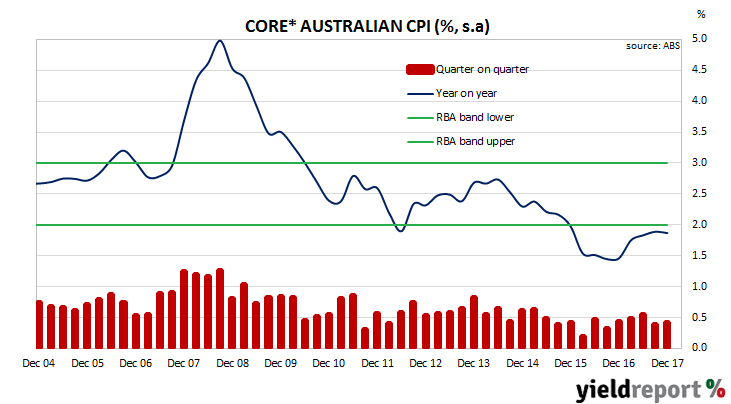

Figures for the December quarter have now been released by the ABS. The headline number was weaker than the expected 0.70%, as were seasonally-adjusted and core inflation figures. Unadjusted inflation was 0.60% for the quarter while seasonally-adjusted inflation also came in at 0.60%. On a 12-month basis, headline consumer inflation recorded 1.90%, up from the September quarter’s comparable figures of 1.80%. On a seasonally-adjusted basis, inflation increased from 1.80% to 2.0%.

Financial markets reacted to the figures by sending bond yields and the local currency lower. Bond yields fell, especially at the short end in a repeat of the bond market response to September’s figures. 3 year yields initially lost 7bps to 2.16% while 10 year bond yields fell 4bps to 2.80% before they closed at 2.20% and 2.82% respectively. The AUD dropped around 0.45 U.S. cents from 81.00 U.S. cents immediately after the report’s release cents before it settled at around 80.60 U.S. cents. Cash futures reduced the chances of the RBA raising the cash rate in 2018, although contracts still imply a 74% chance of an increase before the end of November.

*average of Trimmed Mean & Weighted Median

“Core” inflation measures favoured by the RBA, such as the average of the “trimmed mean” and the “weighted median”, did not change from the September quarter. The average of the two measures were in line with the market’s expected figure 0.40% for the quarter and 1.90% for the year.