Summary: Private sector credit grows by 0.8% in December, above +0.6% expected; annual growth rate rises from 6.6% to 7.2%; business lending “key factor” driving credit surge; credit growth likely “robust over coming months” but headwinds building; business loans account for nearly half net growth, owner-occupier loans another third; investor lending accelerates, personal loans down.

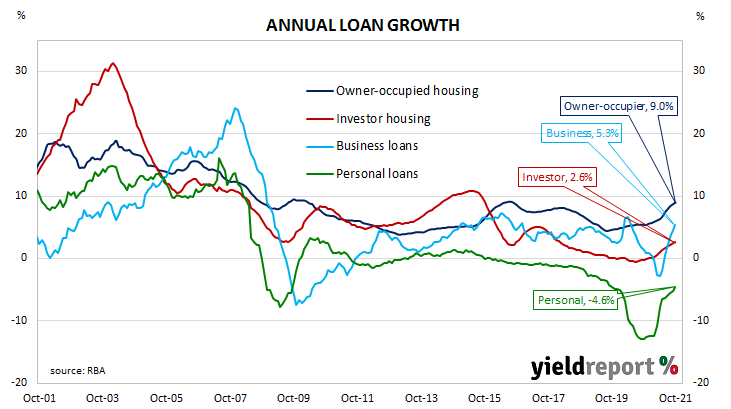

The pace of lending to the non-bank private sector by financial institutions in Australia followed a steady-but-gradual downtrend from late-2015 through to early 2020 before hitting what appears to be a nadir in March 2021. Recent months’ figures indicate the downtrend is over and annual growth rates are now above the peak rate seen in the middle of the last economic expansion.

According to the latest RBA figures, private sector credit growth increased by 0.8% in December. The result was above the generally expected figure of 0.6% but lower than November’s 1.0% increase after it was revised up. On an annual basis, the growth rate increased from 6.6% to 7.2%.

“As occurred in early 2020, businesses during the delta outbreak accessed lines of credit to help ease cash flow pressures during lockdown. This was a key factor driving the surge in credit,” said Westpac senior economist Andrew Hanlan.

Commonwealth Government bond yields fell on the day, especially at the short end. By the close of business, the 3-year ACGB yield had shed 10bps to 1.37%, the 10-year yield had lost 4bps to 1.92% while the 20-year yield finished 5bps lower at 2.40%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.05%, remained fairly soft until May. At the end of the day, contract prices implied the cash rate would not exceed the RBA’s 0.10% target rate until April 2022 and then rise to 0.29% by June. February 2023 contracts implied a cash rate of 1.26%.

“We expect credit growth will remain robust over coming months. Headwinds are building however, in particular the business disruption from Omicron and slowing housing market. These should see a deceleration in credit growth from Q2 this year,” said Morgan Stanley Australia equity strategist Chris Read.

Business loans accounted for nearly one half of the net growth over the month, while owner-occupier loans accounted for just over a third. Investor loan growth accelerated while total personal debt shrank.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.8% over the month, in line with November’s increase. The sector’s 12-month growth rate sped up from 9.3% to 9.6%.

Total lending in the business sector grew by 1.1%, well above the long-term monthly average but noticeably less than November’s 1.6% increase. The segment’s annual growth rate increased from 7.3% to 8.4%.

Monthly growth in the investor-lending segment slowed to a halt in early 2018. Shortly into the 2019/20 financial year, monthly growth rates slipped into the red before posting a series of flat or near-flat results until late 2020. Growth rates became positive again from December 2020. In December, net lending grew by 0.5%, slightly faster than November’s 0.4%. The 12-month growth rate accelerated from November’s 3.0% to 3.4%.

Total personal loans fell by 0.8% in December, in contrast to a 0.6% rise in November, taking the annual contraction rate from 3.5% to 3.8%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.