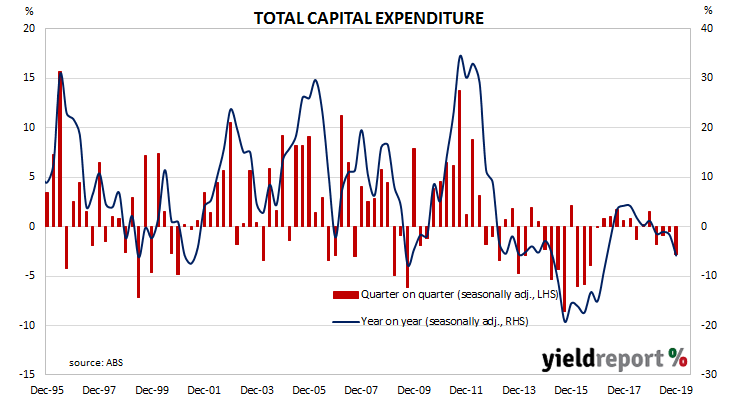

Australia’s capital expenditure (capex) slump was thought to be coming to an end as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. However, contractions in recent quarters have become the norm.

According to the latest ABS figures, seasonally-adjusted private sector capex in the December quarter contracted by 2.8%, well below the +0.5% increase which had been expected and under the September quarter’s revised figure of -0.4%. On a year-on-year basis, total capex contracted by 5.8% after recording an annual rate of -1.6% in the September quarter.

ANZ senior economist Catherine Birch said, “The weakness in Q4 was broad-based across mining, manufacturing and other industries.” Local financial markets reacted by sending bond yields lower. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 5bps to 0.56%, the 10-year yield had dropped by 7bps to 0.85% while the 20-year yield finished 4bps lower at 1.25%.

Local financial markets reacted by sending bond yields lower. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 5bps to 0.56%, the 10-year yield had dropped by 7bps to 0.85% while the 20-year yield finished 4bps lower at 1.25%.

In the cash futures market, traders reacted by hardening their expectations of further official rate cuts in 2020, although a March rate cut was still viewed as quite unlikely. The implied probability of a 25bps cut at the RBA’s March meeting remained unchanged at 11% while April contracts implied a 55% chance of a cut, up from the previous day’s 47%. May 2020 contracts implied another cut in the cash rate target had increased from 76% to 83%. Prices of July contracts continued to have a rate cut fully priced in.