By guest contributor Atchison Consultants

The Australian direct property sector continues to look an attractive investment asset class for those looking for higher yielding returns in a low interest rate environment.

Continuing domestic interest in the asset class together with continued foreign capital inflows are expected to put further downward pressure on capitalisation rates over the next one to two years, with a resultant expected increase in capital values.

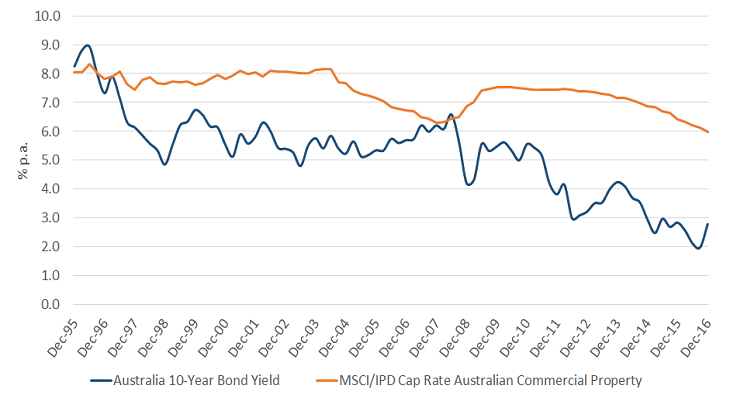

Figure 1 compares the 10-year government bond yield with the market cap rate over 20 years to 31 December 2016.

Cap rate spreads, which can be used as a proxy for yield spreads, continue to remain wide and attractive relative to 10 year Government bond yields, with the spread currently sitting at around 3%.

10 Year Government Bond Yields vs. Australian Commercial Property Capitalisation Rate

Source: RBA, MSCI

We are currently seeing major banks increase lending rates for commercial property borrowers. As the spread in yields narrows between property yields and debt interest rates, we expect this will have a moderating effect on investor demand for property. Capitalisation rates (yields) will flatten and possibly soften, leading to a stabilisation in capital values during the medium term (three to five year period).

We expect that growing tenant demand from increased economic activity resulting will see a flow on effect of increased rental income. This process is expected to be a gradual one over the next couple of years.

Capitalisation rates are below their 10 year long term average of 7.0%, with rate falls still occurring in the office, retail and industrial sectors – with a noticeable downward trend since mid-2015. These falls in capitalisation rates have been primarily driven by strong local and offshore investor demand looking for higher yielding defensive assets, rather than economic conditions or real rental growth.