Summary: Retail sales flat in April, below expectations; UBS: volumes are falling solidly given rising prices; ANZ: discretionary spending weakness may be spreading; largest influences on result from household goods and clothing sales.

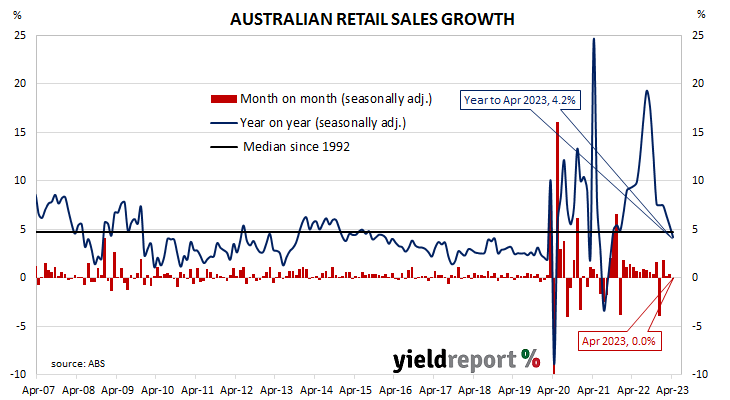

Growth figures of domestic retail sales spent most of the 2010s at levels below the post-1992 average. While economic conditions had been generally favourable, wage growth and inflation rates were low. Expenditures on goods then jumped in the early stages of 2020 as government restrictions severely altered households’ spending habits. Households mostly reverted to their usual patterns as restrictions eased in the latter part of 2020 and throughout 2021.

According to the latest ABS figures, total retail sales remained unchanged in April on a seasonally adjusted basis. The result was below the generally-expected figure of 0.3% as well as March’s 0.4% increase. Sales increased by 4.2% on an annual basis, down from March’s comparable figure of 5.4%.

“Putting aside the issues of monthly volatility and seasonal measurement, the trend has clearly weakened sharply,” said UBS economist George Tharenou, “and now been close to flat for many months, with the level in April 2023 the same as October 2022, which means volumes are falling solidly, given rising prices.”

Commonwealth Government bond yields generally moved modestly higher on the day, ignoring large rises in US Treasury yields overnight. By the close of business, 3-year and 10-year ACGB yields had both added 3bps to 3.44% and 3.74% respectively while the 20-year yield finished 1bp lower at 4.12%.

In the cash futures market, expectations regarding rate cuts in 2024 softened. At the end of the day, contracts implied the cash rate would remain essentially steady at the current rate of 3.82% to average 3.85% in June but then rise to 3.915% in July. February 2024 contracts implied a 3.935% average cash rate while May 2024 contracts implied 3.805%, 1bp less than the current rate.

“While goods-related spending has been soft for some time, dining/takeaway had been holding up well…But dining/takeaway fell 0.2%in April, suggesting weakness may be spreading to more areas of discretionary spending,” ANZ economist Madeline Dunk observed.

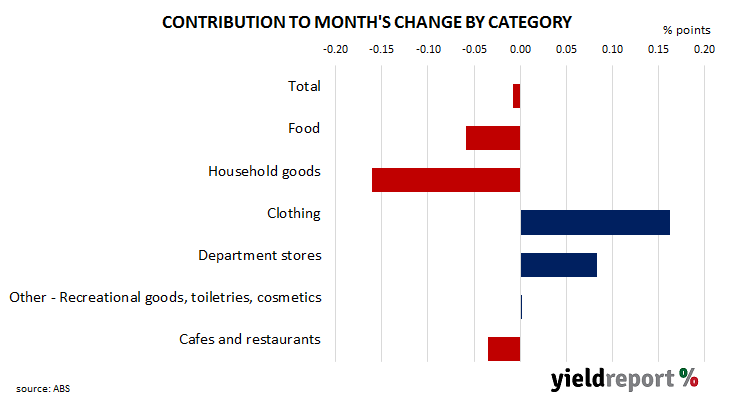

Retail sales are typically segmented into six categories (see below), with the “Food” segment accounting for 40% of total sales. However, the largest influences on the month’s total came from the “Household goods” and “Clothing” segments where sales increased by -1.0% and 1.9% respectively on average over the month.