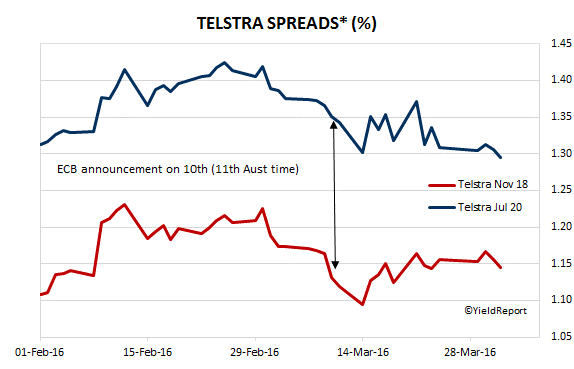

We got another taste of the level of European investor demand for blue chip corporate debt this week when Telstra placed €750 million worth of March 2028 bonds at 20-25bps less than initially indicated. Telstra has an A/A2 credit rating and the substantial discount obtained by the telco group lends credence to the theory the ECB’s asset purchase programme is behind the recent narrowing of corporate spreads over government bonds.

* spread to comparable ACGB

* spread to comparable ACGB

Initially the ECB programme was limited to euro-denominated covered bonds. It was then expanded to state-backed company bonds in 2015 and in February this year it was expanded to investment-grade euro-denominated bonds issued by non-bank corporations established in the euro area. While Telstra does not fit the definition, as yields of bonds which do fit the definition fall, yields on other comparable bonds begin to look relatively more attractive. Because of the ECB buying, the relative shortage of available bonds for other investors has provided Telstra with a windfall benefit on issue.