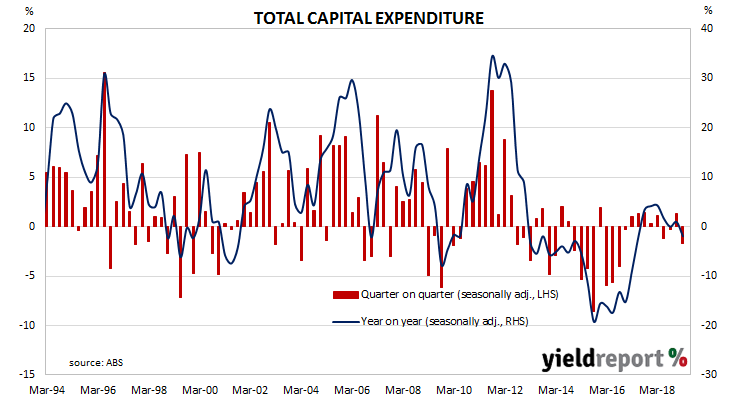

Australia’s capital expenditure (capex) slump was thought to have come to an end in 2018 as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. Even so, two of the quarters in calendar 2018 still had small contractions.

According to the latest ABS figures, seasonally-adjusted private sector capex in the March quarter of 2019 contracted by 1.7%, a deterioration from the December quarter’s +1.3% after revisions and considerably less than the 0.5% increase which had been expected. On a year-on-year basis, the growth rate fell back into the red at -1.9% after recording a revised rate of +1.0% in the December quarter.

Local financial markets reacted by sending bond yields higher while cutting back the likelihood of looser monetary policy, although the April dwelling approvals report may have had something to do with it. By the end of the Australian trading day, 3-year Treasury bond yields were 4bps higher at 1.13%, 10-year yields had gained 5bps to 1.55% and 20-year yields had increased by 4bps to 2.00%. Cash futures prices mostly moved in a direction which implied a lower likelihood of rate cuts in 2019 and 2020 but not in any meaningful way; rate cuts are still the expected outcome. June cash contracts still priced in a 25bps reduction as an 88% chance while August contracts have a cut fully priced in, along with 72% chance of a second, additional cut. November contracts have two rate cuts fully factored in.