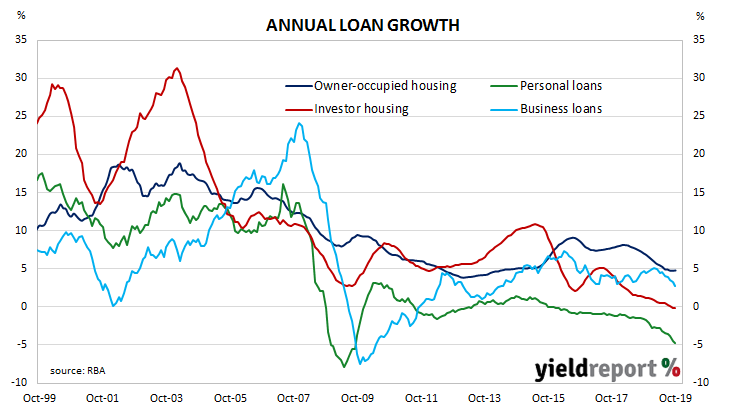

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but then subsequent credit figures put paid to that idea. Despite some optimism emerging in the housing market following the re-election of the Coalition Government in May, lending figures have continued to slow to a rate not that faster than the inflation rate.

According to the latest RBA figures, private sector credit grew by 0.1% in October, well below the +0.3% increase which had been expected and a step down from September’s +0.2%. The annual growth rate continued its downward slide as, this time from September’s figure of 2.7% to 2.5% in October. Lending to owner-occupiers remained solid but restrained while lending in other segments was either flat or contractionary.

ANZ economist Hayden Dimes said, “The lag between new approvals and the stock of credit looks to be almost over, and we could see a sharp pick-up in housing credit growth in coming months.”

Local financial markets reacted by sending bond yields moderately higher while the likelihood of the RBA loosening monetary policy further softened. By the end of the Australian trading day, the 3-year Treasury bond yield had added 2bps to 0.65%, the 10-year yield had gained 4bps to 1.04% and the 20-year yield finished 3bps higher at 1.44%.