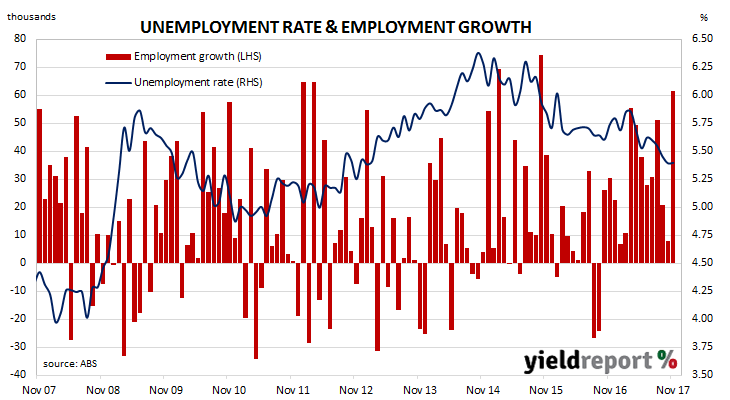

The Australian economy has recorded another month of employment gains, with greater numbers of both full-time and part-time positions. The ABS released employment estimates for November which indicate the total number of people employed in Australia in either full-time or part-time work increased by 61,600. The figure was well in excess of the 19,000 expected.

Bond yields had dropped prior to the report’s release, after yields had fallen in offshore markets overnight. However, once the figures were released at 11.30am, yields jumped, especially on 3 year bonds. By the end of the day, 3 year bond yields were 9bps higher at 2.09% and 10 year bond yields increased by 4bps to 2.59%. In the currency market the Aussie moved higher against the USD and finished around 76.60 U.S. cents.

The unemployment rate came in at 5.4%, the same as in October and the lowest rate since January 2013. Despite the large increase in employment, the unemployment rate remained unchanged as the participation rate jumped from a revised 65.2% to 65.5%.