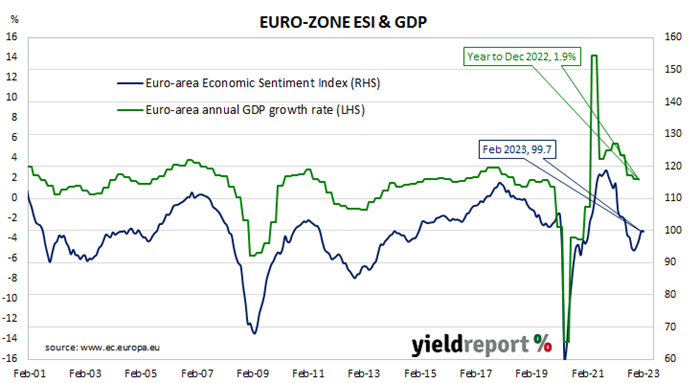

Summary: Euro-zone composite sentiment index down slightly in February, below expectations; readings up in two of five sectors; up in two of four largest euro-zone economies; German, French 10-year yields moderately higher; index implies annual GDP growth rate of 1.3%.

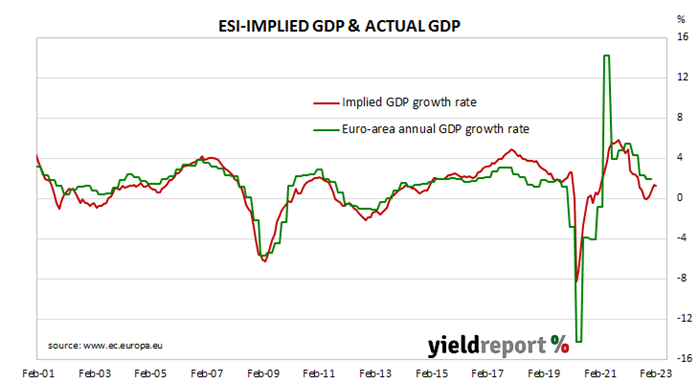

The European Commission’s Economic Sentiment Indicator (ESI) is a composite index comprising five differently weighted sectoral confidence indicators. It is heavily weighted towards confidence surveys from the business sector, with the consumer confidence sub-index only accounting for 20% of the ESI. However, it has a good relationship with euro-zone GDP, although not necessarily as a leading indicator.

The ESI posted a reading of 99.7 in February, below the consensus expectation of 101.0 but just a touch lower than January’s revised reading of 99.8. The decline ended three months of gains but kept the index just under the long-term average. The average reading since 1985 is just under 100.

German and French 10-year bond yields finished the day moderately higher. By the close of business, the German 10-year bund yield had gained 5bps to 2.58% while the French 10-year OAT yield also finished 5bps higher, at 3.05%.

Confidence improved in two of the five sectors of the economy, the consumer sector and retail trade sector, while the industrial and services sectors deteriorated and the construction sector remained steady. On a geographical basis, the ESI decreased in two of the euro-zone’s four largest economies, Italy and Spain, and remained largely unchanged in the other two, France and Germany.

End-of-quarter ESI readings and annual euro-zone GDP growth rates are highly correlated. This latest reading corresponds to a year-to-February GDP growth rate of 1.3%, unchanged from January’s implied growth rate after revisions.