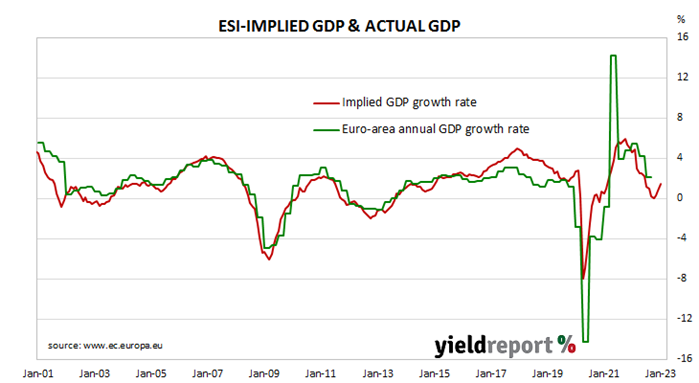

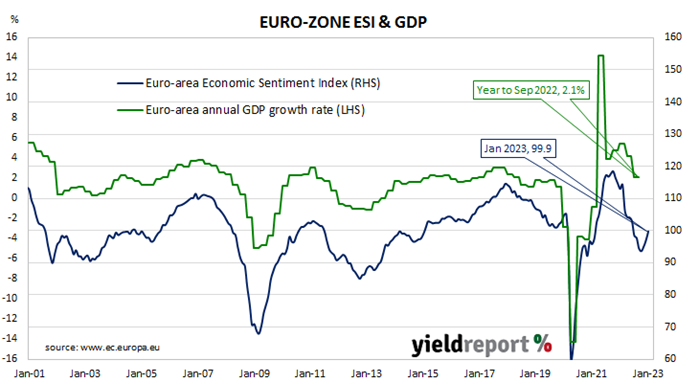

Summary: Euro-zone composite sentiment index up in January, above expectations; readings up in four of five sectors; up in all four largest euro-zone economies; German, French 10-year yields noticeably higher; index implies annual GDP growth rate of 1.5%.

The European Commission’s Economic Sentiment Indicator (ESI) is a composite index comprising five differently weighted sectoral confidence indicators. It is heavily weighted towards confidence surveys from the business sector, with the consumer confidence sub-index only accounting for 20% of the ESI. However, it has a good relationship with euro-zone GDP, although not necessarily as a leading indicator.

The ESI posted a reading of 99.9 in January, above the consensus expectation of 97.0 as well as December’s revised reading of 97.1. The increase marked a third consecutive month of gains for the index, raising it back to the long-term average. The average reading since 1985 is just under 100.

German and French 10-year bond yields finished the day noticeably higher, boosted by Spanish inflation figures which were also higher than expected. By the close of business, the German 10-year bund yield had gained 9bps to 2.31% while the French 10-year OAT yield had added 8bps to 2.77%.

Confidence improved in four of the five sectors of the economy, with the construction sector the only one to experience a deterioration. On a geographical basis, the ESI increased in all four of the euro-zone’s largest economies.

End-of-quarter ESI readings and annual euro-zone GDP growth rates are highly correlated. This latest reading corresponds to a year-to-January GDP growth rate of 1.5%, up from December’s implied growth rate of 0.8%.