Summary: Euro-zone industrial production down 1% in May; contraction triple expected figure; annual growth rate falls, “base effects” still present; production down in all four of euro-zone’s largest economies; supply constraints likely through 2021.

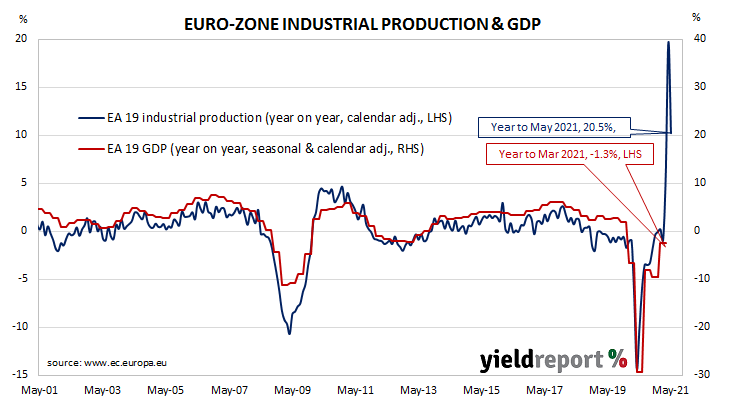

Following a recession in 2009/2010 and the debt-crisis which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in 2016. Growth rates then fluctuated for two years before beginning a steady and persistent slowdown from the start of 2018. That decline was transformed into a plunge in March and April of 2020. However, subsequent months in 2020 and early 2021 produced an almost-complete recovery.

According to the latest figures released by Eurostat, euro-zone industrial production contracted by 1.0% in May on a seasonally-adjusted and calendar-adjusted basis. The fall was triple the 0.3% decrease which had been generally expected and in contrast to April’s 0.6% increase after revisions. On an annual basis, the calendar-adjusted growth rate slowed from April’s revised rate of 39.4% to 20.5%. (Monthly production figures collapsed during the June quarter of 2020, resulting in significantly lower bases for annual calculations. i.e. “base effects”.)

German and French 10-year sovereign bond yields moved lower on the day. By the close of business, The German 10-year bund yield had shed 3bps to -0.32% and the French 10-year OAT yield had lost 2bps to 0.02%.

ANZ economist John Bromhead noted all industrial production categories decreased with the exception of durable goods. He expects an ongoing drag from supply constraints which “are likely to continue to weigh on industrial production until at least the end of the year.”

Industrial production growth contracted in all four of the euro-zone’s four largest economies. Germany’s production contracted by 0.6% while the comparable figures for France, Italy and Spain were -0.3%, -1.5% and -0.8% respectively.