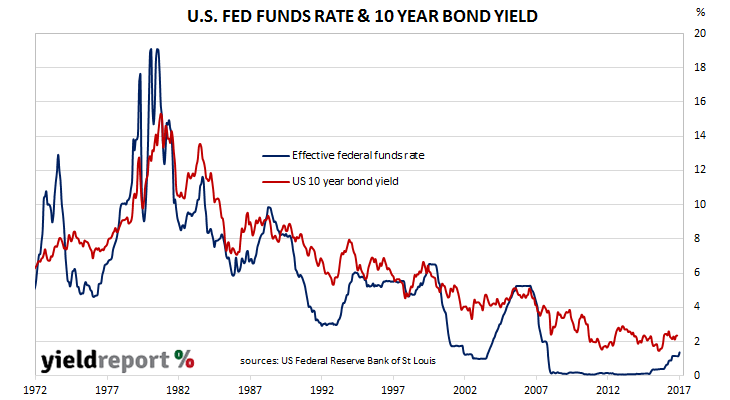

In July 2008, just as the public’s knowledge of the impending mortgage disaster in the U.S was becoming widespread, the federal funds rate was 5.25%. Six months later, it was essentially zero. The U.S. Fed was so concerned about a recession turning into a 1920s style depression, it took the extraordinary step of reducing the cost of borrowing among banks to almost nothing.

As expected, the Federal Open Market Committee (FOMC) announced another 25bps increase to the target range, taking the range to 1.25% to 1.50%. The decision was a reflection of the FOMC’s strategy of “gradual removal of monetary policy accommodation” in light of “solid” GDP growth and a “strong” labour market.

According to projections of FOMC members, there are more rate rises to come. These projections, often referred to as the “dot plots” (because each member’s forecast is represented by a dot plotted over time on a diagram), imply the FOMC expects three rate rises in 2018, taking the federal funds rate range to 2.00%-2.25% by the end of 2018. Another two 25bps rate rises are then expected for 2019.