Summary: Private sector credit shrank in May; business lending drops while owner-occupier lending maintained; investor lending goes backwards faster; “further falls” expected.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but data from the most recent months are starting to look bleak.

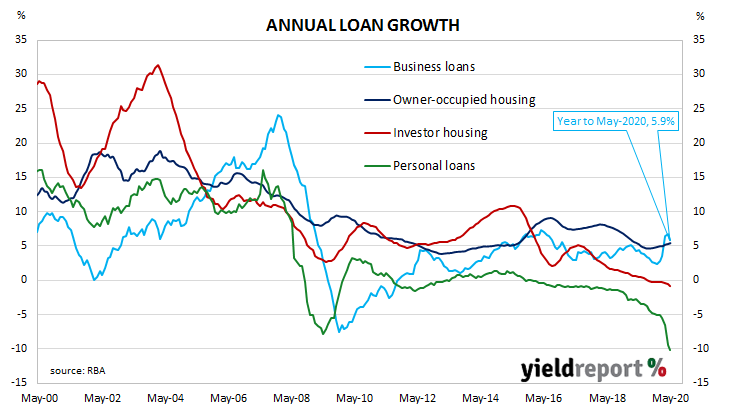

According to the latest RBA figures, private sector credit contracted by 0.1% in May. The result was below 0.0% which had been expected and less than April’s result which was also a flat one. The annual growth rate slowed to 3.1% from April’s comparable rate of 3.6%.

Westpac senior economist Andrew Hanlan said he expected “further falls…”

The result was largely driven by a reduction in business loans, with personal debt and investor housing loans also contracting. Owner-occupier loans continued to grow steadily. Local Treasury bonds yields moved a little lower, largely in line with movements in US Treasury yields in overnight trading. By the end of the Australian trading day, the 3-year Treasury bond yield remained unchanged at 0.28%, the 10-year yield had slipped 1bp to 0.89% while the 20-year yield finished 2bps lower at 1.50%.

Local Treasury bonds yields moved a little lower, largely in line with movements in US Treasury yields in overnight trading. By the end of the Australian trading day, the 3-year Treasury bond yield remained unchanged at 0.28%, the 10-year yield had slipped 1bp to 0.89% while the 20-year yield finished 2bps lower at 1.50%.

In the cash futures market, expectations of a rate cut firmed a touch. At the close of business, July contracts implied a rate cut down to zero as a 62% chance, up from the previous day’s 59%. August contracts implied a 53% chance of such a move, unchanged. Contract prices of months in the remainder of 2020 and through to late-2021 implied similar probabilities, ranging between 33% and 55%.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.5% over the month, the same rate as in March and April. The sector’s 12-month growth rate ticked up to 5.4% from April’s rate of 5.3%.

However, ANZ economist Hayden Dimes thinks this will not last. “With a weak labour market and subdued wage growth, we anticipate owner-occupier credit growth will slow and then turn negative over the coming 12 months.”

Growth rates in the business sector had been slowing until they picked up in the first quarter, with an especially large increase in March. In May, business credit contracted by 0.6%, a noticeable fall from April’s revised growth rate of 0.2%. The segment’s annual growth rate slowed from April’s revised rate of 6.7% to 5.9%.