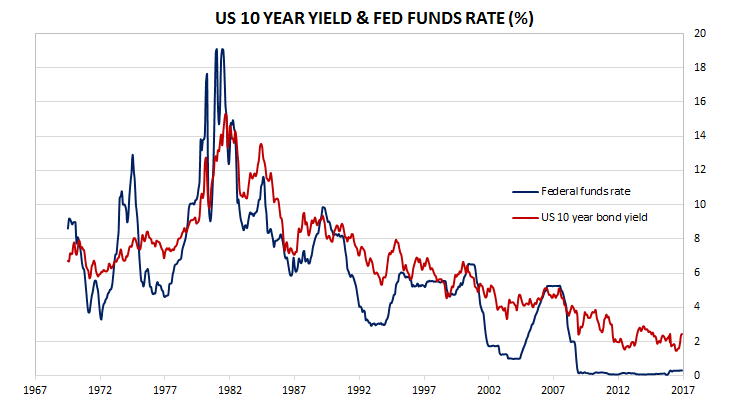

As expected, the US Fed left its official rate steady. The Fed’s interest rate setting committee, known as the Federal Open Markets Committee (FOMC) kept the Federal Funds target rate at its range of 0.50% to 0.75%. US bond yields initially fell after markets took the view there was little chance of a rate rise any time soon, but ended the day 1bp higher at 2.47%.

The language used in the accompanying statement changed in a slightly hawkish manner. According to NAB’s Tapas Strickland, “…the Fed seemingly upgraded its inflation outlook ever so slightly, noting that inflation ‘will rise to 2%’…The Fed also noted the recent improvement in consumer and business sentiment of late.”

However, Westpac economist Eliot Clarke said the statement did not change his view of the path of US official interest rates in 2017 or further out. “Changes made to the statement’s language offered no justification to alter our view that the Committee will look to raise the Fed Funds Rate twice this year and another two times in 2018…”

Even though Fed officials as senior as Janet Yellen have alluded to three rises per year through to the end of 2019, markets are still expecting a fairly measured pace of increases. According to cash futures pricing, March is viewed as about a 1 in 8 chance for a rate rise and even May is rated as 1 in 3.

However, economists typically are taking a more hawkish view. UBS economist Samuel Coffin said, “We continue to expect two 25 bps hikes this year, but better capex, faster employment growth, or a stimulative enough fiscal package could shift our expectations to three.” Goldman Sachs were more definitive; “We see limited implications for the near-term policy outlook, and continue to assign a 35% chance that the committee raises rates as soon as the March 14-15 meeting. Our modal forecast remains three hikes this year, at the June, September and December FOMC meetings…”